Despite the recent bout of losses in bond funds, they have not lost their ability to generate returns.

Bonds or bond funds have a place in asset allocation for their ability to provide stability and predictability to the portfolio. In a healthy market, it can deliver about a 1% real rate of return and if it does so, this should be a cause for satisfaction. The reason we are re-visiting this premise is the recent bout of losses that investors have experienced in bond funds. Was it something that should have been expected or factored in assumptions while allocating assets?

Bonds have not lost their ability to generate returns – the question is how much and for how long. And here lies the secret to its positioning. If a particular bond has a coupon that is higher than the prevailing market rate for a safe (read G-Sec/AAA) investment, there is bound to be a premium for it which the investors will obtain on sale as capital appreciation.

Conversely, if the coupon is lesser than the prevailing market then there will be a discount on sale to compensate the buyer for lower interest rate on the bond. It is pertinent to understand that this premium or discount is notional till the instrument is sold. So if an investor simply holds on to the bond till maturity instead of trading it, he will not experience any capital gains or losses but just get the coupon rate.

The lesson here is that “if the investor holds on till maturity, mark to market is not pertinent.” Based on the time horizon of investor’s need, matching bond maturity should be chosen. Or in the case of a bond fund, a similar average maturity. If an investor wants long term rate even though he needs money before maturity, then he has to take the risk of marking to market on sale before maturity. Arbitraging between long term and short term thus carries a risk of loss if rates move up in the interim. Another lesson here is - “match time horizon of the need to maturity when choosing the bond fund to avoid risk of loss.”

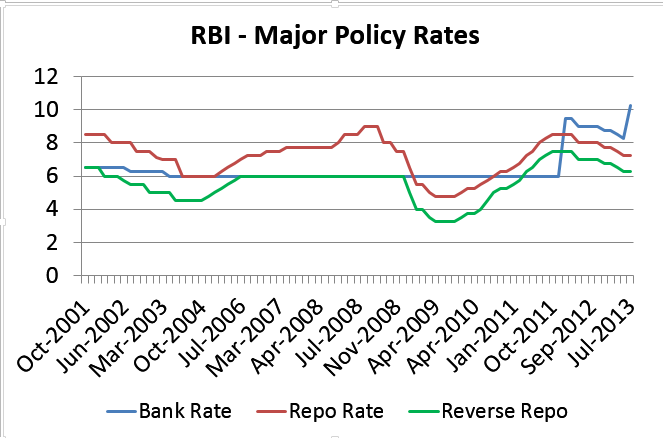

What about the converse? Can one profit from changes in rates? Since 2001, we have seen more than one cycle of interest rate changes. We are in the middle of third cycle and were expecting a secular trend of falling rates when monetary policy was tightened to control speculation on the rupee.

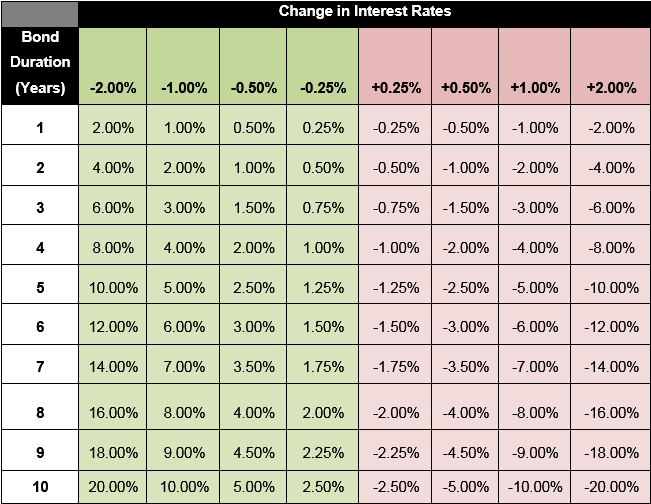

An investment made at the top of an interest rate cycle will yield large capital gains if sold on the downward slope. And any investment made at the bottom of a cycle will result in losses on the way up. So the lesson here is – “the more the change, the greater the impact on bond price.” Not only should we look at change in rate, but also the residual maturity of the bond. The longer it is, the greater the impact, as the table below shows. The lower part of the table illustrates the impact on price for a given change in interest rate for a particular bond duration:

This is the price risk that an investor carries if he intends to mark-to-market the bond price. In the recent crisis, some investors were overweight on long duration bond funds and hence experienced high losses on NAV. Ideally, if the fund manager has not changed the composition of his portfolio in the meanwhile, the investor will eventually receive as returns, the YTM of the portfolio (less expenses) if he stays on for the average maturity of the fund. Regardless of the fund manager’s ability to judge a situation, he may be forced to sell if he is faced with large redemption requests, typically from institutional investors. Hence lesson four would be – “choose a fund with more of retail investors than institutional investors to reduce volatility induced by redemptions.”

If one wants to reduce price risk when marked to market, an easy solution is to stick to Fixed Maturity Plans (FMPs). No price risk – be content with the yield on the portfolio due to coupon. Lesson five - “ladder up” the portfolio i.e. to have bonds or bond funds with differing average maturities, say, 33% in liquid or short term; 33% in medium term funds and 33% in long term bond funds.

This is a diversification across duration to reduce risk of price volatility. But investors will have to take on what is called as re-investment risk which is, re-investment at a lower interest rate. There is always a price to be paid for safety and this has to be explained to the investor prior to the investment. I have found that the best guard against investor dis-satisfaction is to educate him sufficiently so that he appreciates your advice and rationale.

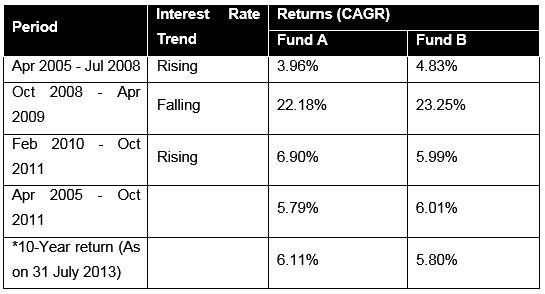

A long term investor in a well-managed bond fund will not lose, if he stays on to the average maturity of the portfolio. No super-returns, no losses. The performance of two reputed funds is below:

*The yield on a 10 year G-Sec, 10 years ago was 7% pa.

Dynamic bond funds claim to manage the rate cycle in their portfolio – the performance or promise depends entirely on the skill and the knowledge of the manager. The call to include these in a portfolio comes with this disclaimer!

The views expressed in this article are solely of the author and do not necessarily reflect the views of Cafemutual.