ICRA’s recent study finds that investors could get additional returns of up to 1.67% post tax in liquid funds over savings bank accounts. In fact, the difference between the returns of savings account and liquid funds could go up to 3% pre tax.

As banks cut deposit rates due to declining interest rate environment and surplus liquidity after demonetisation, liquid funds fetched higher returns compared to savings accounts, says the report.

Other aspects of liquid funds that distributors can play on are instant redemption facility and no exit loads, says the report.

In terms of risk, the report says that liquid funds are relatively less volatile than other mutual funds due to high credit quality and short term nature of its underlying instruments.

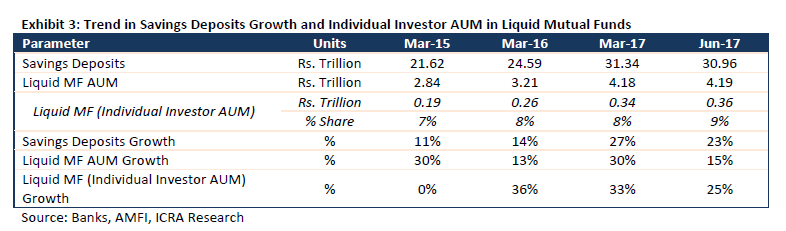

The rating agency also finds that individual investors have been increasingly investing in liquid funds. The share of individual investors’ investments in liquid mutual funds has increased by 34% in just two years. In the meantime, investments in savings bank accounts grew by 20%.

As individuals currently hold only a small portion of their assets in liquid funds, distributors should encourage their clients to invest in liquid funds. Most retail investors invest in mutual fund though equity funds, says the report. “With the arbitrage between liquid mutual funds and savings rate and that between liquid mutual funds and bulk deposit rates likely to continue, the pace of incremental inflows into liquid mutual funds is expected to increase over the near to medium term. With AMFI also taking significant initiatives to introduce mutual funds to all classes of investors, ICRA expects retail investors to deploy a higher proportion of their incremental funds into liquid funds,” the report says.