It is not just debt funds, which are getting popular among direct investors, equity funds too have been receiving healthy inflows through direct plans.

MFDEX data that covers 96% of industry shows that mutual fund industry has recorded highest gross sales of Rs.62,192 in equity funds through direct plans between January and June 2018. On the other hand, the industry has witnessed gross sales of Rs.45,606 crore in equity funds through individual distributors in the first half of 2018.

CAMS collates data from other R&T agents such as Karvy Computershare, Franklin Templeton and Sundaram BNP Paribas to make MFDEX report.

While direct plans accounted for 25% of gross sales in equity funds, the IFA channel contributed 19% in the equity gross sales in the first six months of the current calendar year.

Industry experts believe that direct plans have three broad categories – direct retail, direct institutional and direct RIA. A lot of action has been happening in the direct institutional and direct RIAs space. While many large institutional investors invest in arbitrage funds through direct plans, many RIAs have been recommending their clients to invest in mutual funds through direct plans. However, gross sales in direct retail is still marginal, say experts.

However, if we include all the distribution channels such as individual distributors, national distributors (NDs), banks and others (robo advisors and overseas distributors), the industry has recorded gross sales of Rs.1.83 lakh crore in equity funds.

Among distribution channels, IFAs top the charts with Rs.45606 crore gross sales in equity funds. Private banks followed IFAs with gross sales of Rs.43417 crore in equity funds.

In addition, national distributors recorded gross sales of Rs.35,435 crore in equity funds. Many individual distributors work with NDs like NJ India and Prudent under sub-broking model. The data shows that both IFAs and NDs account for 33% (19% and 14% respectively) of gross equity sales.

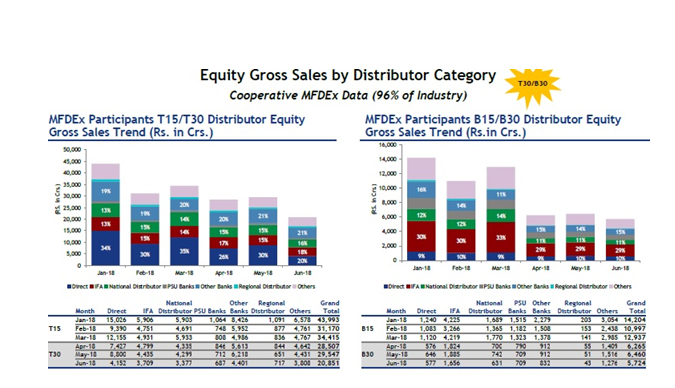

In terms of geographical distribution of gross sales, IFAs recorded highest gross sales in both T15 and B15 cities among distribution channels.

Overall, in T30 cities, direct investors share in equity gross sales is 20%. IFAs and national distributors follow direct investors with 18% and 16% share in equity gross sales. However, in B30 cities, IFAs share in equity gross sales is 29%, PSU banks 12% and national distributors at 11%. Direct investors share in equity gross sales is 10% in B30 cities.

|

Distributor Type |

Gross equity sales |

|

IFAs |

45,606 |

|

NDs |

35,435 |

|

Regional distributors |

5,662 |

|

PSU Banks |

11,093 |

|

Other banks |

43,417 |

|

Direct |

62,192 |

|

Other |

41,665 |

|

Total |

2,45,070 |