In the last bi-monthly monetary policy review meeting held on the 4th October 2019, the six-member Monetary Policy Committee (MPC) of the Reserve Bank of India (RBI) jointly agreed on a rate cut of 25 basis points, placing the repo rate to 5.15% with immediate effect.

This collective decision was taken after assessing a host of global and domestic undercurrents–– mainly GDP growth, liquidity conditions, and inflation.

The MPC also retained the “accommodative stance” as long as it is necessary to revive economic growth, which clearly has lost momentum and acknowledged by RBI.

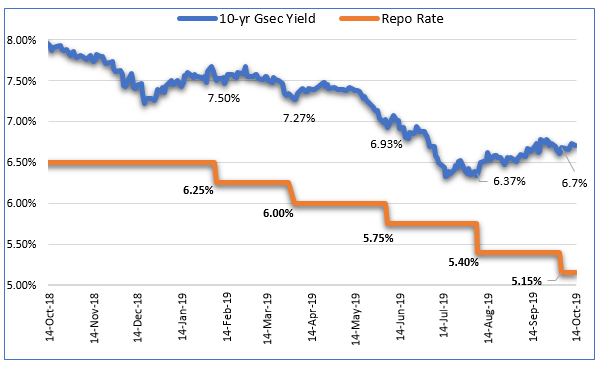

The RBI also observed that monetary transmission has remained staggered and incomplete. Against the cumulative policy repo rate reduction of 110 bps from February-August 2019, the weighted average lending rate (WALR) on fresh rupee loans of commercial banks declined by 29 bps.

Graph 1: How have 10-year G-sec yields pursuant to policy repo rate cuts…

Data as of October 14, 2019

(Source: RBI, PersonalFN Research)

Path to inflation and interest rates…

According to the RBI, the inflation trajectory will be guided by several factors, mainly the following:

- Food inflation, mainly prices of vegetables and pulses

- Demand conditions, which are expected to remain weak

- Crude oil price, which is expected to remain volatile in the near-term (on the backdrop of slowing global demand and geopolitical tensions)

- Three-month and one-year ahead inflation expectations of households polled by the Reserve Bank

- Financial markets, which are expected to remain volatile

Taking into consideration the aforesaid factors and the impact of recent policy rate cuts, the CPI inflation projection is revised slightly upwards by the RBI to 3.4% for Q2:2019-20, while projections are retained at 3.5-3.7% for H2:2019-20 and 3.6% for Q1:2020-21, with risks evenly balanced.

The future course of RBI’s policy rate actions will depend on the incoming data prints, mainly inflation.

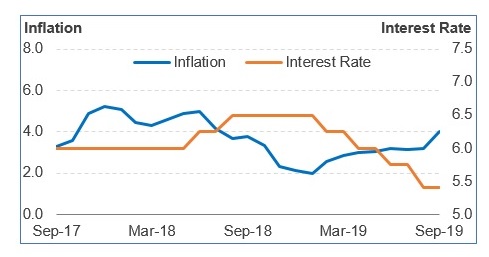

Graph 2: CPI inflation has moved up in the last couple of months, but so far not beyond RBI’s comfort zone

Data as of September 2019

(Source: MOSPI, RBI, PersonalFN Research)

CPI inflation for September 2019 has come fastened to 3.99% (data released in October 2019) from 3.21% in August 2019 due to an increase in prices of food items, mainly-- vegetables, pulses, meat, fish, and beverages. Similarly, inflation in ‘fuel & light’ category too has declined to -2.18%.

Even ‘core CPI inflation’ ––which excludes food and fuel prices––eased marginally to 4.20% in August 2019 (data released in September 2019) from 4.24% in the previous month due to sluggish demand. Cumulatively, CPI inflation for the period April-July FY2020 declined to 3.11% compared with 4.25% in April-May FY2019.

So, are we in the last leg of a policy repo rate cut cycle?

Well, looks like. The RBI has reduced policy repo rates by good 135 bps since February 2019 to support growth.

Given that the CPI inflation is still within RBI’s comfort range, perhaps another 25 bps policy repo rate cut appears cannot be ruled out in the next i.e. the 5th bi-monthly monetary policy statement for 2019-20 (scheduled in December 2019). But beyond that, the RBI may also be compelled to look at the interest of depositors.

The approach to follow while investing in debt mutual funds now…

In such a scenario, when IFAs advise debt mutual fund schemes to clients/investors, selecting the sub-category with care and prudence is important. Investing aggressively at the longer end of the yield curve could prove less rewarding and risky (may encounter high volatility) in the foreseeable future.

Thus, it is better to deploy money in shorter maturity papers via shorter duration funds. But IFAs should advise and approach even short-term debt funds with eyes wide open and closely look at the portfolio characteristics and quality of the scheme. In the recent past, many debt mutual funds across maturity profiles were holding downgraded and toxic debt papers which increases the investment risk.

So, prefer the safety of principal over returns. Stick to debt mutual funds where the fund manager isn’t chasing returns by taking higher credit risk and assess the risk appetite and investment time horizon of your client/investor while investing in debt funds.

While advising short-term debt funds, IFAs should ensure that the client/investor has an investment horizon of at least 2-3 years.

For an investment horizon of 3 to 6 months, ultra-short duration funds would be suitable. And if the client/investor has a time horizon of less than 3 months, he/she better off investing in overnight funds or a liquid fund.

Don't forget that investing in debt funds is not risk-free!

Remember, a sensible and astute investment strategy paves the path to wealth creation.

Jimmy A Patel is MD & CEO Quantum Mutual Fund. The views expressed in this article are solely of the author and do not necessarily reflect the views of Cafemutual.