Portfolio construction can be either through direct investments in the instruments i.e. equities or bonds or through an investment vehicle. In direct investments, it is solely on the investor to research, execute and track, or at most he can avail of advice e.g. advisory PMS.

Among investment vehicles, there are multiple options e.g. mutual funds, PMS, AIFs, etc. In this, ULIPs usually do not have a top of the mind recall. There are reasons for this mind-block, particularly the unpleasant experience of the past, in terms of high front-loading charges (aka allocation charges) and relatively higher recurring expenses.

However, things have improved now, which makes ULIP a feasible investment vehicle. We will discuss the arguments here, which should clear the mental hurdles towards accepting this for a place in the portfolio construct.

- The allocation costs have come down drastically so much so that in some ULIPs it has become zero (for premiums above Rs. 3 lakh). Generally, costs are there, but there are benefits including life cover. Many insurance providers nowadays provide loyalty additions and fund booster at certain intervals, over and above the fund value.

- ULIPs provides a wrap account with multiple funds in one product. Majority of ULIP providers have cash fund, bond fund, multi cap fund, large cap fund and so on to choose from. Depending on market conditions, one can switch between asset classes without having to worry about switch cost, exit loads and tax treatment. Switching is app and web based, making it convenient.

- New age ULIPs provide flexibility to withdraw funds after 5 years. Clients having SIP horizons of 5 years or longer can choose ULIP for portfolio construct. If required, it is possible to avail of loans against ULIPs. Loan amount can be up to 90% of policy value.

- ULIPs allow tax-free wealth creation with the benefit of section 10(10D) of Income Tax Act 1961, against capital gains tax of 20% after indexation applicable on fixed income mutual funds and 10% tax applicable on equities and equity mutual funds.

- After PPF, this is the only product in the country that follows principle of exempt- exempt-exempt during savings, growth and withdrawal phase against taxed-exempt- taxed in mutual funds (except ELSS where it is EET) and taxed-taxed-taxed in PMS.

- We tend to forget that ULIPs also provide life cover. If one compares the mortality cost in ULIPs, charged on sum-at-risk, with premium of an equivalent reducing-term plan, cost may be lower in ULIPs. The reason is, in ULIPs the insurance company takes its cost from fund management charges whereas in term plan it is added to cost in premiums paid, over and above mortality cost.

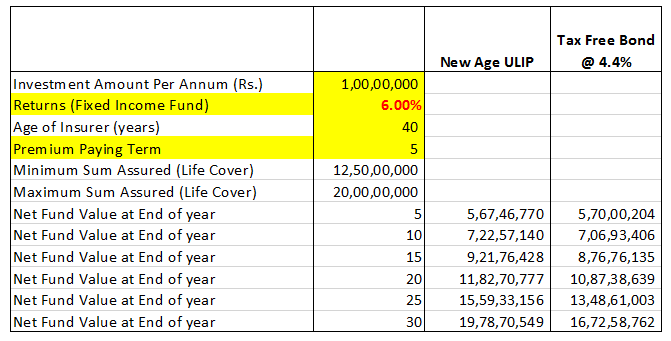

Comparative: fund growth

We present here, two comparatives on fund growth:

Table 1: Assuming 6% CAGR in ULIP and 4.4% in tax-free bond

Since ULIPs are tax free, like tax-free bonds, this table shows the higher fund value, at the assumed growth rate.

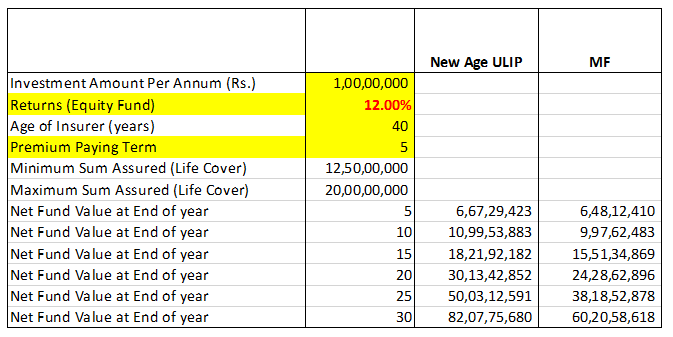

Table 2: Assuming 12% CAGR in ULIP and MF

The differential in returns between ULIPs and MFs is due to:

- Differential in fund management charges

- 0.95% against 0.5% - 2% of Debt Mutual Funds depending on sub-category of debt fund

- 1.35% against 1.5% - 2.25% of Equity Mutual Funds

- Differential in taxation

- ULIPs are tax free under section 10(10D) whereas mutual funds are taxed at 10% LTCG for equity MFs and 20% post-indexation for debt MFs.

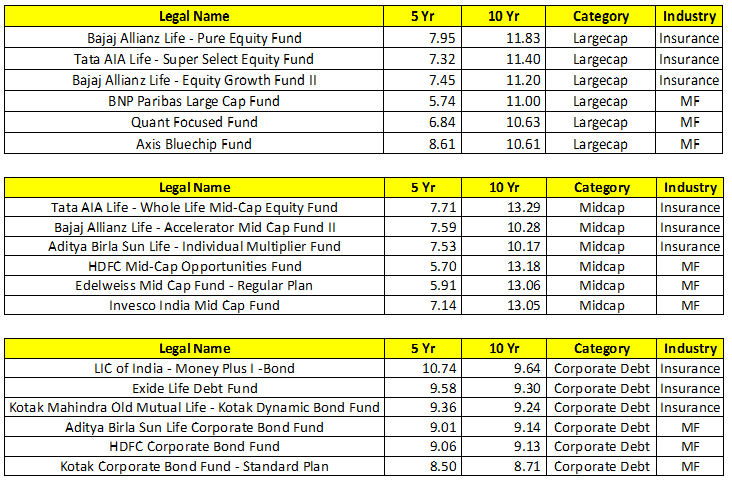

Comparative: Fund performance

We present here, performance of top-performing ULIP and MF funds:

Performance numbers as of August 13th, 2020 by SATCO WEALTH internal research.

Conclusion

New-age ULIPs are an excellent tool to build future wealth for any financial goal, including retirement and savings for children. Depending on the goals and horizon, ULIPs can be utilized along with other investment vehicles like MF or PMS. The efficacy in terms of performance, cost and taxation is evident.

Deepak Jaggi is Co-founder and managing director at Satco Wealth Managers. He can be reached on deepak.jaggi@satcowealth.com.

The views expressed in this article are solely of the author and do not necessarily reflect the views of Cafemutual.