SEBI has issued a concept paper on introduction of swing pricing mechanism in debt mutual funds that aims to discourage short term traders and protect the interest of existing investors especially during difficult times like market dislocation.

Swing pricing is adjustment of NAV such that if outflow is higher than pre-determined level, the NAV goes down for investors redeeming MF units. Similarly, the NAV price goes up if investors invest more than pre-determined level.

Currently, swing pricing has two types – full swing and partial swing. While NAV is adjusted on every calculation day in full swing (applicable during market dislocation), partial swing is applicable only if a scheme witnesses high inflows/outflows on a given day compared to pre-determined level. Partial swing can be applicable on normal market scenario. SEBI hints to implement hybrid model which would be combination of both – full and partial swings.

To start with, SEBI may introduce swing pricing mechanism in riskier debt schemes. The market regulator may look to extent such an option in equity funds in the later stage.

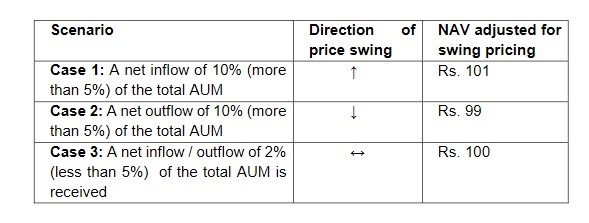

Here is the illustration on possible scenario:

Considering a scheme having NAV of Rs.100 and swing threshold of 5% of the net inflow/outflow of the scheme, here are three scenario of NAV adjustment:

Pros

- Helps fund houses to achieve fairness in treatment of entering and exiting investors

- No first move advantage i.e. investors redeeming earlier sensing market dislocation cannot benefit at the cost of other investors

- Reduces risk of impact of high redemption pressure on scheme

Cons

- Challenge in determining appropriate parameters for swing pricing

- May increase redemption pressure before its implementation

- If large and small investors redeem on a same day, the latter can get lower NAV

SEBI’s argument

- Prevalent in all developed markets like US, France, Hong Kong and Luxemburg

- Swing pricing can address issue of heightened redemption pressure especially during volatile market conditions

- Protects investors from underperformance of a scheme due to significant outflows

- Addresses the issue of first mover advantage

- Deals with liquidity issue in secondary bond markets

- Lowers daily NAV volatility

Proposed framework

- Implementation of hybrid model i.e. partial swing during normal course of market and full swing during market dislocation

- A pre-defined framework to implement swing pricing. For instance – redemption of up Rs.2 lakh for all unitholders and up to Rs.5 lakh for senior citizens can be exempted from swing pricing

- AMCs can choose to levy higher swing factor

- SEBI to determine ‘market dislocation’ after consultation with AMFI

You can comment on following aspects

- If there is a need to introduce swing pricing mechanism?

- Whether full swing/partial swing or hybrid model be applicable?

- If swing pricing can be facilitated in normal times, market dislocation or both?

- If it should be made mandatory for all open end debt funds?

- What should be the swing threshold?

- Should exemption be given to a set of investors?

You can read the concept paper by clicking here. Also, you can submit your responses to Harshad Patil, Assistant General Manager at swingpricing@sebi.gov.in and harshadp@sebi.gov.in.