Listen to this article

PGIM India is one of the fastest growing mutual funds in India. In fact, its assets went up sharply over the last one year. What are three factors that have contributed to this?

We follow GARP that is growth at reasonable price, with a focus on margin of safety. We also ensure a strict filtering process to identify the businesses that are a part of our portfolio. Over the years, this process has ensured a disciplined thought process and hence, we have achieved continuity and consistency in performance.

Further, we have a varied spread of fund offerings including a few funds on the international platform managed by our parent entity which has given investors an opportunity to participate not only in the domestic markets but also the international markets adding to diversification of their portfolios.

Lastly, a well curated sales strategy of focusing across different channels at different points in time along with consistency in performance, communication and branding has helped broaden our set of active partners across channels.

Of late, balanced advantage funds have been getting popular among investors. What are the key reasons for this rising interest?

Balanced Advantage Funds (BAFs) strike a chord with investors and distributors/advisors on a few things like active asset allocation, better risk adjusted returns & efficient taxation. Essentially, BAFs intend to buy low & sell high which is what most investors and distributors would want to do to achieve better returns at lower risk. With the pandemic our life, work and commute has become more hybrid. Inherent flexibility is a core advantage. And so, hybrid investments have naturally begun to be more favoured.

Balanced advantage funds have gained a lot of traction. These funds are designed to actively manage asset allocation with the help of pre-defined formula for better outcome. However, globally, we have seen these funds do not work. Do you think these funds are good for Indian investors?

It’s important to set expectations correctly and not advise them as an alternative to long only equity investments but rather an addition to the core portfolios to provide stability with superior risk adjusted returns. The fact that most money entering our industry is allocated towards traditional fixed return instruments which arguably are no longer as lucrative, ensures that a product segment with lower volatility along with better investment outcomes is available.

In mutual fund industry, we have products for every time frame – for instance, flexi cap funds are good for long term while fixed income funds are better for short to medium term goals. Where does BAF fit? Does investor really need BAFs?

BAFs as a category aims at generating superior risk adjusted returns for the investor. In simple terms, it is a core allocation product for a portfolio alongside funds like a flexi cap and a mid-cap but serving a purpose of providing stability in returns for the investor along with active asset allocation, lower volatility and efficient taxation. Apart from time frame, risk appetite is important too. For a whole category of investors therefore, BAFs are a fill it, shut it, forget it kind of solution for any medium to long time frame.

PGIM India has a popular offering in the hybrid space — the PGIM India BAF. It is known for its distinct asset allocation approach called DAAAF. How is this model different from the approach taken by other fund houses?

Price to earnings ratio (P/E) is the simplest to understand and a more relevant valuation methodology as it explains the larger part of the market. The PGIM India Balanced Advantage Fund uses the variation of the P/E i.e. the difference between the current P/E and historical P/E (The 20-day average P/E from the 15 Year rolling average P/E). This is important because with the changing landscape of interest rates and the overall macro environment, the valuation premium that equity enjoys is different, which may not be captured by static models. To summarize, the model we follow for PGIM India Balanced Advantage Fund works on a fundamental indicator of the P/E ratio along with a dynamic variation based model which ensures that it stays relevant into the future.

The PGIM India BAF is still quite new for us to evaluate its performance. How has the fund performed in back testing across cycles?

The back testing results of the model, when tested for a period beginning January 2007 to May 2022, the model has delivered returns of 8% and above for about 75% of the time on a 3 year lumpsum investment and over 92% of the time for a 5 year lumpsum investment on a monthly rolling return basis. All of the above outcomes have been delivered with relatively lower volatility and hence, better risk adjusted returns.

Many MFDs say that they already recommend aggressive hybrid and conservative hybrid funds to their clients and find no merit in adding another fund to their recommendation list. Why do you feel that there is space for PGIM India BAF in their clients’ portfolio?

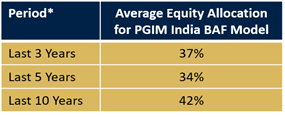

PGIM India BAF model is transparent and isn’t a black box as the model works on dynamic data and isn’t static. BAFs offer lower volatility than an aggressive hybrid and better taxation and return profile than a conservative hybrid. BAF as a strategy solves for the need of active allocations (buy low – sell high) along with the benefit of equity taxation to an investor. Essentially, the investment strategy in PGIM India Balanced Advantage Fund ensures allocation from a floor of 30% to 100% directional equity depending on the variation model. If you see, the back-testing results of the model underlying the PGIM India Balanced Advantage Fund, has delivered as below;