The revision in computation of dividend distribution tax (DDT) for debt funds proposed in the Union Budget FY2014-15 becomes effective from October 1. Fund houses pay DDT for dividend income distributed by debt funds which is tax free in the hands of investors.

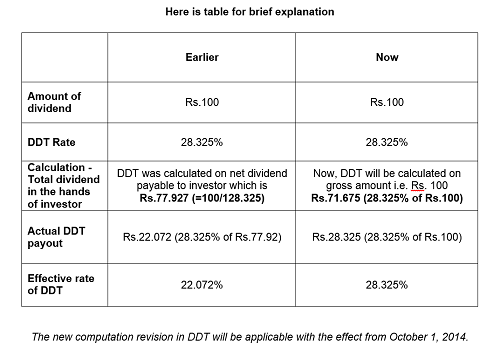

Debt funds currently pay DDT of 25%+ 10% surcharge + 3% cess on net basis when they distribute income to resident individuals. Calculation on net basis reduces the actual pay out to 22%. Finance minister has retained the DDT rate; however, the computation process has changed. Now, fund houses are required to pay DDT on gross basis which will hike the actual DDT payout.

With the proposed revision in computation, the DDT on debt funds will now be 28.32% for retail investors. For corporates, the DDT will be 33.99% in liquid and debt funds.

So, how does it affect your clients? Since the DDT is 28.325% now, the post-tax return will be less.

Fund houses and distributors are likely to promote growth plans of debt funds from now on.

Experts say there is no point opting for dividend payout option for an individual falling under 10% and 20% tax bracket if investment horizon is less than three years. However, investors who fall in the highest tax slab of 20% can still opt for dividend option since they have to pay 28.32% in debt funds compared to 30.90% in bank fixed deposit. Short term capital gains are taxed as per the investor’s tax slab.

If your client’s time horizon is more than three years, you can advise them to invest in growth options of debt funds as they can benefit by paying a less tax of 20% with indexation.

An alternative is to opt for systematic withdrawal plan (SWP) if your clients need a regular income. SWPs are more tax efficient. Investors belonging to the highest tax slab will have to pay 10.3% on the SWP income compared to 30.9% for withdrawing while bank fixed deposits.