Listen to this article

You have close to 25 years of experience in the fixed income market. What are your two key learnings from this market?

- A clear investment philosophy that stays consistent over time and market cycles is extremely important and well appreciated by investors.

- Ensuring that the two sides viz. liabilities (investor type and concentration) and assets (credit quality and liquidity) are in sync with each other and not compromised due to the pressure to perform

With US bonds reaching new highs and rising geopolitical tension, what is your near term outlook on fixed income funds?

Markets globally have been volatile over the last few weeks. We have seen sharp movements in bond yields and currency. 10-year US Treasury yields hit 4.80% (on the back of a stronger than expected non-farm payroll data), with a segment of market participants expecting yields to breach 5%. Back home also we saw 10-year G-Sec hitting 6.85% and Rupee breaching 87 recently.

While markets continue to trade on the long USD idea, a fair bit of negativity is already priced in. What transpires over the next few months, in terms of policies/tariffs etc. will remain a key monitorable, and will give further direction to asset classes, but in case the announcements turn out to be softer, USD rally could moderate auguring well for EM currencies and bonds.

On rates front, with recent data showing economic strength, US markets could remain higher for longer and the Federal Open Market Committee (FOMC) might have their work cut out resulting in a shallow easing cycle. For other economies, while risks remain on policies introduced by the new regime in the US along with FOMC rate trajectory, US Treasury rates and any Chinese Yuan (CNY) depreciation, the central banks across geographies will act basis their domestic macro factors. From an India perspective, some key macro factors are aligning creating a conducive environment for a beginning of a rate easing cycle. We continue to remain positive on our outlook on Indian bond markets and expect interest rates to move lower, supporting our long duration bias across portfolios.

There have been no rate cuts despite the fact that inflation is in control. Currently, the central bank focuses on keeping inflation within their comfort zone. However, in this process, many experts feel that growth has been compromised. What’s your take on this?

Inflation has seen some sharp movements in the last few months, predominantly due to food price variations. Persistent shocks to food prices detract the disinflationary process, which has curbed the Monetary Policy Committee or MPC’s ability to act on rates. However, given the recent softening in food prices, we expect headline inflation to align with RBI’s estimates over the next few months creating space for the MPC to act.

The recent weak GDP growth was a huge surprise for economists as well as market players; however, attributing weakness in growth completely to RBI inaction might not be appropriate. With inflation risks remaining elevated on the back of unrelenting food prices, RBI remained justifiably ambivalent on rate actions. Some extent of regulatory driven slowdown in credit growth was indeed required to bridge the gap between credit and deposit growth. Meanwhile, private capex has not picked up and weak Government spending during the election periods (both at the Center and key states) culminated in domestic slowdown. However, the growth inflation balance is expected to improve over the next few months as inflation retraces back to sub-5% levels. This would free up RBI’s ability to respond better to downside growth risks.

There is substantial traction in the credit market. Do you think that MFDs should look at credit funds now? If yes, why?

Last few years has seen an uptick in credit growth. Newer channels to create accrual products have also picked up, which have seen significant traction. While some investor segments might prefer to look at accrual products as part of their allocation, we believe that given the strong domestic macro fundamentals, along with a favourable demand supply dynamics and an imminent rate easing cycle, there is potential to create alpha through generating capital gains across traditional products that can potentially outperform credit-oriented funds, without taking any significant credit risks. We would recommend investors to capture this structural move lower in rates to generate alpha and once the rate easing cycle is over, move to higher accrual products like credit-oriented funds depending on their risk appetite.

Talking about the debt funds, the majority of fixed income fund categories did not generate alpha over the 1 and 3 year period. In fact, many MFDs now believe in recommending debt-oriented hybrid funds or passive funds for debt allocation. Your comments.

During the pandemic period and subsequently, repo rate was cut by the MPC to a low of 4% and liquidity was in abundance which augured well for bond yields. But as inflation started picking up, central banks globally had to start raising policy rates to counter inflation. Domestically also policy rates were hiked by 250 bps between May 2022 and Feb 2023. This correspondingly saw a sharp rise in bond yields as well, resulting in underperformance over a 3-year period.

However, over a 1-year period various categories of fixed income funds have generated 8%-10% returns, even before commencement of a rate easing cycle in India, as yields have fallen due to various factors, including FPI index related inflows, favourable demand supply dynamics, improving domestic macro factors, which are expected to continue going forward. With expectations building up of easing in policy rates, we recommend investors to look at active debt strategies which have the potential to generate alpha, basis their risk appetite and investment horizon.

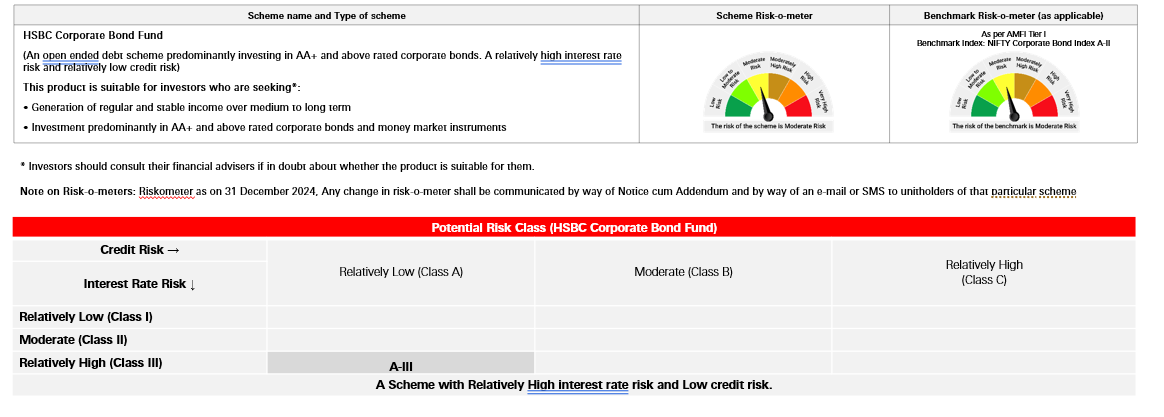

AMFI data shows that your corporate bond fund has done well in the last one year. What has contributed to this?

Our Corporate Bond Fund is positioned predominantly in the 3-5 year segment of the yield curve. Yields of 3-5 year government securities are lower by around 40 bps and 3-5 yr corporate bond yields are lower by around 30 bps during the year. On an average, over the last year, we have remained overweight duration positioning in our fund compared to peers, which has aided in performance.

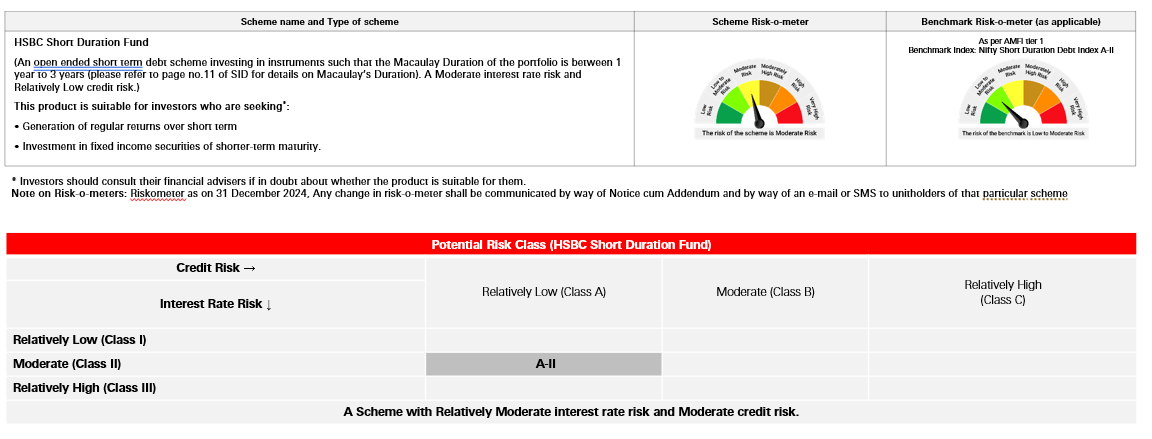

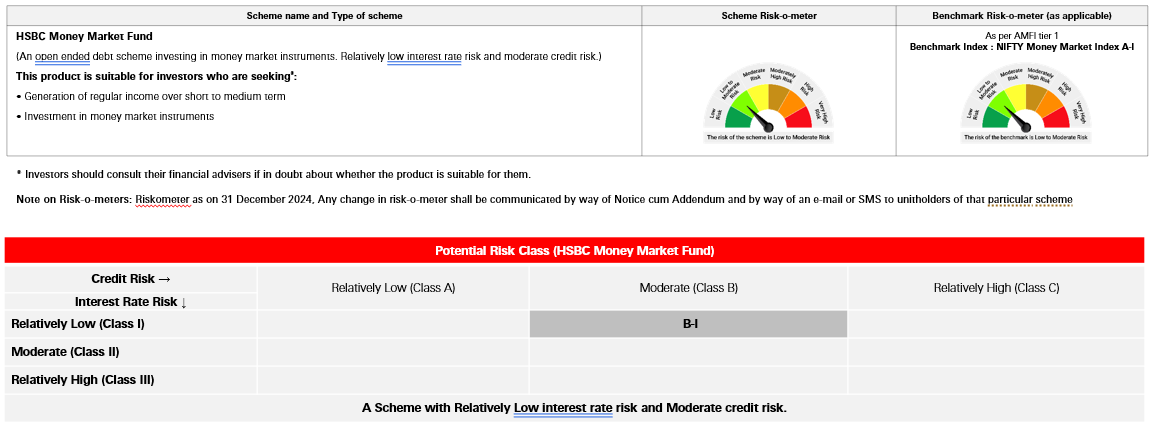

A few of your funds like short term funds and money market funds have delivered at par returns. What are you doing to regain its performance momentum?

We are maintaining a more nimble footed and active duration strategy in our Short Duration Fund. Unlike our peers, we continue to maintain a 100% AAA portfolio, in line with our investment strategy for this fund. With an active duration strategy, appropriate asset allocation mix and yield curve play, we believe the fund is well positioned to outperform in the coming years.

We have aligned our Money Market Fund strategy with the market, by adopting an active duration strategy and a favourable portfolio yield, which has already resulted in improvement in its relative performance over the past few quarters.

Which categories of debt funds should MFDs recommend to clients?

The coming year is bound to be eventful and exciting from an investment perspective. We believe two investment strategies remain relevant, the benefits of which will unfold over the course of the year.

- While rates are expected to move lower across the maturity spectrum, the yield curve is likely to steepen significantly over the course of the year, as short end yields move lower on the back of positive liquidity and rate cuts. Hence, we remain positive on schemes with 3-5 year AAA corporate bonds, which may benefit from this curve steepening, rate cuts and spread compression.

- Given the favourable demand supply dynamics in the government bond market due to steady growth of long-only investor segment, along with the government’s focus on fiscal consolidation and strong macro fundamentals, we remain positive on our outlook for the longer end of government securities curve.

Based on the two key investment strategies suggested above, we believe the following categories can be considered as possible avenues to generate alpha over the course of the year.

- Mutual fund categories with core investments in the 3-5 year AAA corporate bond segment viz. short duration funds, medium duration funds and corporate bond funds can be positioned to benefit from curve steepening and spread compression.

- Actively managed long duration funds with investments in the longer end of G-Sec curve, viz. Gilt funds and dynamic bond funds can be positioned to benefit from positive G-Sec demand supply dynamics.

Product Labelling and PRC

All data as of December 31, 2024.

Note: Views provided above are based on information in public domain and subject to change. Investors are requested to consult their financial advisor for any investment decisions. Past performance may or may not be sustained in the future and is not indicative of future results.

Source: Bloomberg, RBI & HSBC MF Research estimates as on January 31, 2025 or as latest available