Since the entry load ban, the economics of the fund advisory business has undergone a sea change. Many IFAs who were catering to clients investing low amounts are beginning to part ways or are less interested in entertaining such clients. Advisors contend that handling such investors has become unviable as commissions don’t cover operational costs. Moreover, many advisors feel that retail investors are reluctant to shell out a fee.

As a result, some have pruned their clientele and are only on boarding those clients who bring a certain ticket size, say Rs 10 lakh. “We need more manpower, computers, stationary to cater to retail clients. We have stopped accepting fresh money from retail clients below a certain threshold,” says a Mumbai based advisor who has restructured his model.

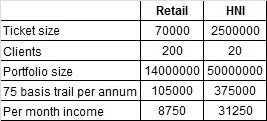

Take for instance, an advisor who has 200 retail clients with an average portfolio worth Rs 70,000. The total portfolio size becomes Rs 1.40 crore and the advisor would earn Rs 1,05,000 per annum on a 75 basis points trail, which works out to Rs 8750 per month. Servicing 200 clients with a monthly revenue of Rs 8,750 per month could be a tall order when an office boy costs Rs 6,000 per month in Mumbai.

On the other hand, an advisor would have earned Rs 31250 per month if were to handle 20 HNIs with a portfolio of Rs 25 lakh each. Many advisors and those particularly in metros have found that advising a few clients with a bigger portfolio is better than catering to a large clientele.

Income from Retail versus HNI

For start-up IFAs, building a retail model looks tough at this juncture unless they invest their own money for few years before they break even.

Retail not that bad

Not all is bad with retail model. Retail assets are generally sticky. As per AMFI data (March 2012), 62% of retail equity assets remained invested in equity funds for more than 24 months, as compared to 40% in HNI category. “Retail investors remain with you for a long time and are less demanding as compared to HNIs. Distributors in small towns still accept applications worth Rs 5, 000. I don’t think retail investors will even opt for direct plans,” observes Ramesh Bhat of IFA Galaxy.

Vinayak Sapre, a Mumbai based financial advisor says that IFAs who want to build a retail base should advise SIPs which are autopilot in nature. He observes that many IFAs cater to retail clients but they can’t simply abandon them because these clients have been investing through them for a long time. “One needs to establish himself as a solution provider and not just a product seller; otherwise client looks at you as an agent. Adopting technology could help cater to retail clients. People who are investing Rs 1,000 per month have the capacity to invest Rs 5000 per month also but IFAs need to ask for it,” says Vinayak.

IFAs could also provide investors an option to invest through their websites to minimise transaction costs.

With the additional incentive for AMCs to tap small town investors, IFAs from these towns could hope for a higher brokerage which could further enhance retail market, at least in small towns. With the possibility of a higher commission payout, they will be looking to make the most out of it.