Listen to this article

Private credit provides an alternative source of financing for businesses with unique funding needs and irregular cash flows. Such financing takes place via asset managers involving a private credit/alternative investment fund (AIF) that intermediates between the ultimate lender and borrower.

Globally, the private credit market started gaining pace after the financial crisis in 2008 as banks retreated from riskier lending to small and mid-sized businesses and to companies backed by private equity. A decade later, a massive debt crisis in India caused the RBI to put a tight leash on NBFCs enabling private credit players to expand their horizon.

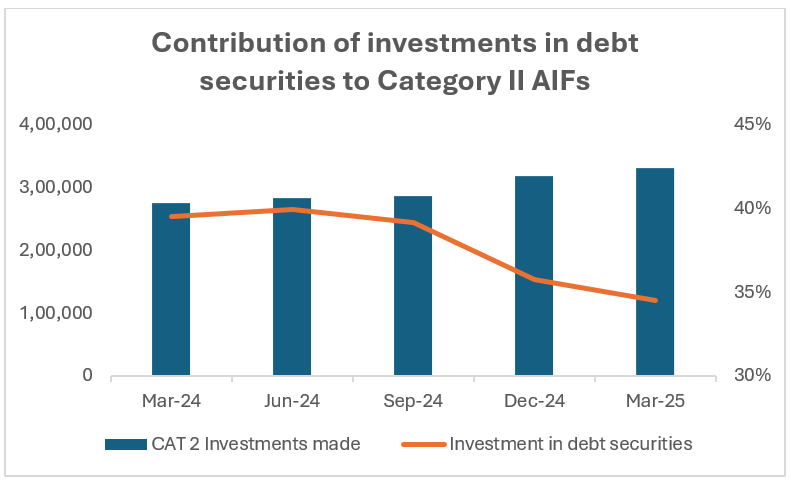

At a broader level, domestic AIFs have continued to exhibit secular growth in the recent past with majority of the incremental funds raised in Category II and Category III. In Category III, the ratio of investments in listed securities to unlisted securities is significantly higher (~95:5) with equities predominating such investments. Meanwhile, the growth in Cat II funds has been contributed by the Private Credit segment with debt investments contributing 35-40% to the segment as per data released by SEBI.

Source: SEBI

Private Credit AIFs have also become increasingly attractive to HNIs, family offices and institutions to generate real returns. However, investing in the space requires a highly professional fund manager involving a dedicated team with regional touchpoints for primary and non-syndicated deal sourcing and possessing the capability and tech for high-level risk management and monitoring.

The strategies adopted by Private Credit AIFs are determined by the type of entities the funds invest in and their stage in the business cycle. Broadly, the following are the strategies adopted by such funds:

- Structured Debt: Structured Debt funds use a mix of fixed-income and equity strategies and provide a degree of both capital protection and capital appreciation to investors. These types of debt funds invest the majority of the portfolio in fixed-income securities and offer principal repayment along with interest payments. Some structured debt funds also imply pooling similar debt obligations and selling off the resulting cash flows via a securitization process. The pooled assets are repackaged as interest-bearing securities, which are issued to investors.

- Performing Credit: Performing Credit strategies seek to make debt investments in mid-market operating companies. While banks meet their standard funding needs, private credit AIFs who understand this space and can take a ground-up approach stand to benefit by offering structured solutions for specific requirements such as working capital correction, last mile capex and product development financing, among others. The investee companies in such funds have strong business models owned by accomplished promoters and are typically repaying debt through operational cashflows. These strategies seek to generate high risk-adjusted returns while at the same time providing predictability and stability.

- Venture Debt: Venture Debt strategies invest in companies that already have venture capital backing to provide them funding for working capital or capital expenses, such as equipment purchases. Unlike Performing Credit, venture debt is available to start-ups and growth companies that might not have positive cash flows or significant assets to use as collateral.

- Distressed Debt: Distressed Debt aka Special Situations strategies invest in mid-market companies that have an element of distress, dislocation, or dysfunction and are perceived to be undervalued by the manager. The investment is done with the intention to either gain control or exert influence over the investee firm. The returns are dependent on the manager’s ability to exit the business after a successful turnaround.