Why did Franklin Templeton MF resort to winding up of debt funds if the fund house could have temporarily suspended redemption?

The fund house has borrowed funds to meet the redemption pressure during lockdown 1.0.

Currently, SEBI allows fund houses to borrow funds up to 20% of the AUM to meet redemption requirements. The fund house borrowed 30% in a few schemes after taking SEBI’s approval during lockdown 1.0.

However, the government has extended the lockdown adding to the woes of the fund house. The fund house continued to witness heightened redemption volumes and reduced inflows. Also, high levels of borrowing could have magnified the effects of any negative credit events in the portfolio.

In a press conference, Sanjay Sapre, President, Franklin Templeton India said that the fund house had explored the possibility of suspending redemptions until market conditions stabilize without winding up the schemes. However, conditions for such a suspension under the current regulatory framework, such as a maximum suspension period of 10 working days (in 90 days) and the requirement to honour redemptions up to Rs.2 lakh per day per investor, rendered this approach unviable to meet the severe and sustained impact of the current crisis, he added.

Also, since the fund house has to honour redemptions under any circumstances, fund manager could be forced to sell the relatively better instrument in the portfolio to meet redemption. As a result, the proportion of relatively inferior securities could have increased in the portfolio affecting investors who did not exit. The fund house said that they have taken this decision to protect the value for all investors.

What happens when schemes wind up?

These schemes will no longer open for any fresh subscription and redemption with effect from April 23, 2020. This includes purchases or redemptions through SIPs, STPs and SWPs. That means, it would not be possible for your clients to do STP in equity funds if they have invested in any of these schemes. All in all, you can say that the entire fund becomes a segregated portfolio.

How will the funds return money?

The schemes will return the money to unitholders in a staggered manner based on scheme’s portfolio maturity. The fund house will either wait for maturity of securities or sell securities at reasonable amount without raising impact cost. This essentially means, funds having short term debt securities like short term funds and ultra-short term funds will return the money more quickly than credit funds.

How long will the schemes take to liquidate assets?

The fund house said that it aims to liquidate the portfolio holdings at the earliest opportunity. Once the market recovers from the current Covid-19 situation, early exits via sale/prepayment will be actively explored with a view to facilitate repayment prior to the maturity of the portfolio investments, the fund house added.

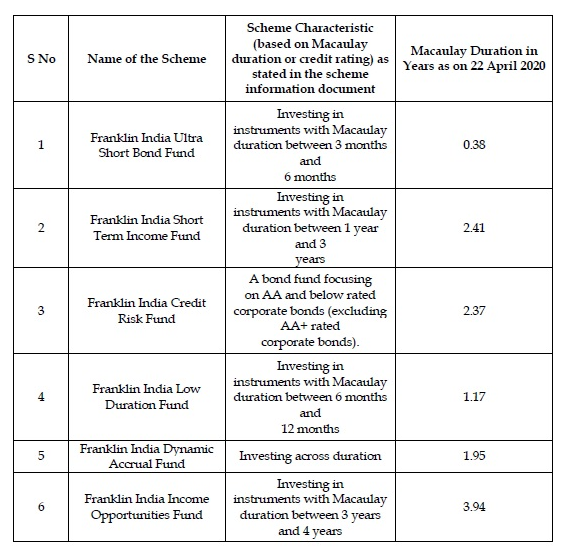

However, SEBI has specified the macaulay duration of each scheme category which indicates maximum time these funds can take to liquidate. Here is the list:

What would be taxation?

Taxation depends on date of realization of securities and holding period of your clients. Simply put, the amount received by investors are in the form of redemption of units and would be taxed as capital gain in the hands of investors depending on the period of their investment in the scheme.

What would happen to side-pocketing exercised in these funds?

The side-pocketing pocketing exercised in these schemes will remain intact.

What about the expenses charged to these funds?

The fund house will not charge any management fees for these funds. However, expenses as permitted under SEBI regulation will continue to be charged to the funds. These are generally in the nature of audit fees, custody fees, fund running expenses, etc.