Principal Small Cap Fund has completed a year. Tell us about the journey of the fund so far?

Principal Small Cap Fund has completed one year in May 2020. The fund has outperformed its benchmark (the NIFTY SmallCap TRI) as well as other broader market cap indices. More than 2/3rd of the fund’s portfolio is invested in small cap companies. The fund has a well-diversified portfolio across companies and sectors. Portfolio has been diversified across 18 sectors. Over the last one year, we increased allocation to industrial products, fertilizers and consumer goods and reduced allocation from metals, textiles and energy.

Tell us about the fund management strategy of this fund. How is this fund different from other small cap funds?

Principal Small Cap fund follows a bottom up stock selection investment philosophy. Typically, we look for investment opportunities in quality stocks with growth opportunities and available at an attractive valuation where we foresee growth at a reasonable price. According to a Morningstar analysis, the portfolio has 58% allocation to growth stocks, 18% allocation to value stocks and balance 24% to blend stocks as on May 29, 2020. The endeavour is to invest in robust businesses, with strong operating metrics and which have reasonably good growth visibility.

The small-cap segment has been hit badly. How do you see the valuations for these segments?

The sell-off in the equities has been broad based across market capitalizations and sectors leading to multi year lows for many stocks. With the recent correction, there are several good quality businesses that are available at attractive prices in each segment of the market.

Which businesses in small cap segment according to you have turned attractive after the sharp correction?

The recent market correction has brought almost all sectors in the fair and attractive valuation zone. We expect a consolidation and a continuing shift form the unorganized to the organized segments of the economy and companies with less leverage, a strong balance sheet, steady and robust business models and good management quality to gain as they are likely to weather the storm better than others.

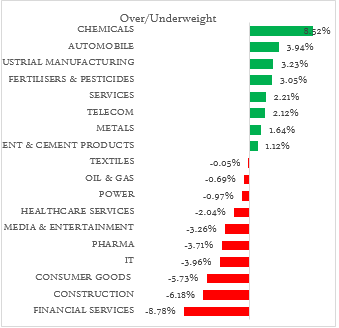

Can you share some thoughts on your portfolio construction strategy? Your views on sectors and business overweight and underweight positions in fund?

We follow a bottom up approach to stock selection and endeavour to build a diversified portfolio with exposure across sectors and industries. The universe of stocks comprises companies that have a robust business model and enjoy a sustainable competitive advantages with earnings that are expected to grow better than other companies in their respective sector.

We follow a bottom up approach to stock selection and endeavour to build a diversified portfolio with exposure across sectors and industries. The universe of stocks comprises companies that have a robust business model and enjoy a sustainable competitive advantages with earnings that are expected to grow better than other companies in their respective sector.

Currently the chemical sector is overweight in the portfolio. Other overweight sectors included industrial manufacturing and fertilizers & pesticides. Higher exposure to industrial products is based on our expectation that the demand for building materials would likely revive especially due to the revival in rural consumption and housing demand. Rural India is not likely to get impacted from Covid19, given the huge support from the government and migrants returning to villages from cities thereby improving labour availability for agriculture – this is a significant positive for the fertilizers & pesticides sector.

Financial services, construction and consumer goods were top underweight sectors. We maintained underweight in financial services as we believe that smaller players in this sector could be negatively impacted in the near term, particularly NBFCs lending to SMEs, consumer goods and commercial vehicles. Banks could witness another round of stress if lockdown continues for a long time. IT (Software) was also a top underweight sector. We believe that H1FY21 would be significantly impacted due to clients reducing spends especially on the discretionary side of the business.

Why should advisors recommend this scheme to their clients?

Principal Small Cap Fund portfolio is well diversified across sectors. The companies under this portfolio are high quality businesses with proven track record over a long period of time and strong balance sheets. Advisors should recommend this fund based on their assessment of the risk appetite and the financial goals of the investor.