Dhawal Dalal EVP, Head - Fixed Income, DSP BlackRock makes a

strong case for investing in government bonds for a time horizon of three to

six months.

Recent reduction in Cash Reserve Ratio (CRR) by the

Reserve Bank of India (RBI) has been viewed positively by the market

participants.

Recent reduction in Cash Reserve Ratio (CRR) by the

Reserve Bank of India (RBI) has been viewed positively by the market

participants.

Although the government bond price action after the CRR cut suggested that some market participants were disappointed as they had been expecting more from the RBI, we sense a shift in the RBI’s monetary policy approach going forward.

We believe that it is important to recognize the subtle change in the RBI’s approach and its likely impact on the government bond prices in the mid-term.

Although the RBI is unlikely to reduce the Repo Rate due to increasing inflationary pressures, we believe that the RBI is gradually loosening its hawkish stance on monetary policy by stealth. We think it will continue to do more of that in the next three months as well.

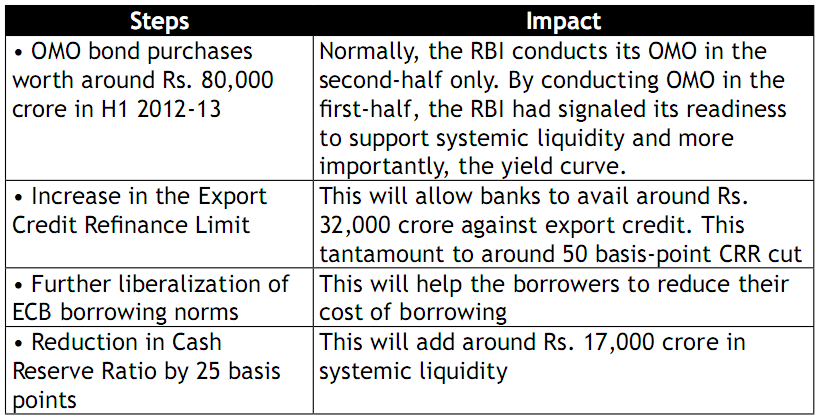

Some recent steps taken by the RBI in this financial year and their impact on the bond market are as follows:

All these developments bode well for government bonds over the medium- term.

With the benchmark 10Y yield @ 8.16% pa, government bonds seem to offer excellent value. At these levels, government bonds are not pricing in any rate cut expectations. Therefore, we believe that this represents a great entry point to invest in liquid government bonds with an investment horizon of 3 to 6M.

To be fair, there are two near-term risks in the market. One, prospective increase in the government borrowing program by around Rs. 75,000 crore due to likely upward revision in the fiscal deficit for FY2012-13. Second, possible sovereign credit rating downgrade by rating agencies.

These risks, as and when they materialize, are likely to push yields up by around 15-25 basis points. However, we believe that investors should take advantage of the development and further increase their exposure to liquid government bonds.

The benchmark 10Y government bond yield will trend lower over the medium-term. The question in everyone’s mind is - can it go below 8% level?

We believe that the benchmark 10Y government bond yield will trade below 8% level only when the RBI cuts the benchmark Repo Rate, or if there is a substantial improvement in the systematic liquidity.

Going by the current developments, if the government is able to maintain the momentum and push for more reforms which help the economy gain traction and contain fiscal deficit through various means, then there is a greater chance that the RBI will consider reducing the Repo Rate, notwithstanding the inflationary pressures. We think that RBI may reduce the Repo Rate by 25 bps in 1Q2013.

As and when that happens, we believe that the benchmark

10Y yield may dip below 8% and may trade between 7.75% -8% pa range. With deteriorating

credit environment and

prospects of widening

in credit spreads, we

believe that the

government bonds offer

attractive medium-term investment

opportunity with comparatively lower credit risk and better liquidity. The RBI

is also likely

to conduct more

OMO bond purchases

worth Rs. 1,00,000 crore in the

second-half of the year to support systemic liquidity and M3 growth. At the

same time, the government appears to be sincere

in its efforts to address fscal

defcit and its approach for fscal consolidation, by pushing for the crucial

diesel price hike last week.

The data is based on our internal analysis and may change as subsequent conditions vary. DSP BlackRock Mutual Fund has used information that is publicly available including information developed in-house. Information gathered and used in this material is believed to be from reliable sources. The Fund/AMC however does not warrant the accuracy, reasonableness and/or completeness of any information.