Listen to this article

Ask any active fund votary about passive funds and they will often list three disadvantages of passive funds — lack of downside protection, compulsion to pick losers and the absence of a skilled management team. Their argument surely has substance but are they that big a problem that you should avoid passive funds completely?

At the Cafemutual Passives Conference 2022, Navi AMC CEO Hari Shyamsunder looked at each of the arguments against passive funds to see how substantial they are. Here's what he found out in each case.

Problem 1: Passive funds are risky

In an active fund, the fund manager can save investments during a market correction by making timely intervention and selling off a part of the holding. However, this is not possible in passive funds and they keep going down with the markets.

However, as per Shyamsunder, data fails to establish that active funds are good at protecting funds from a downslide. "Data gives a mixed signal. There is nothing to show that active funds are able to consistently offer downside protection," he said.

Problem 2: Passive funds pick losers

It is true but not a big problem, says Shyamsunder who believes that owning the winners is more important than worrying about the losers. "When the plan is to create wealth over a long term, the focus should be to make money. Past data shows that only a small set of stocks have done extremely well in the long run. Missing out on such stocks can be very detrimental to wealth creation. Index funds are the right way to capture all the wealth creation opportunities," he said.

Problem 3: Lack of skilled management

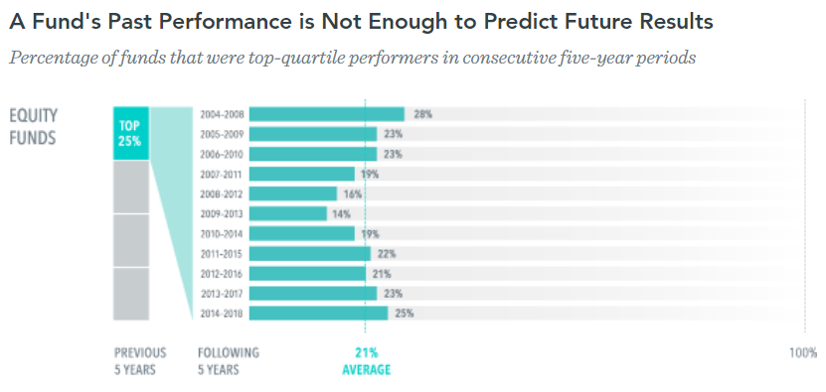

Active funds have a highly skilled team to steer the fund in the right direction. That's not the case in passive funds. This brings us to the question — how important is human mind in wealth creation? Here's what data, as shared by Shyamsunder, shows:

The best way is to look at the funds’ consistency. Data shows that only 40% active funds of the top 25% performers during 2013-2016 maintained their lead when five-year data was considered. When another three years were taken into account, none of the 2013-2016 performers were there in the picture.

This shows that though some actively managed funds perform really well, they find it hard to do it consistently.

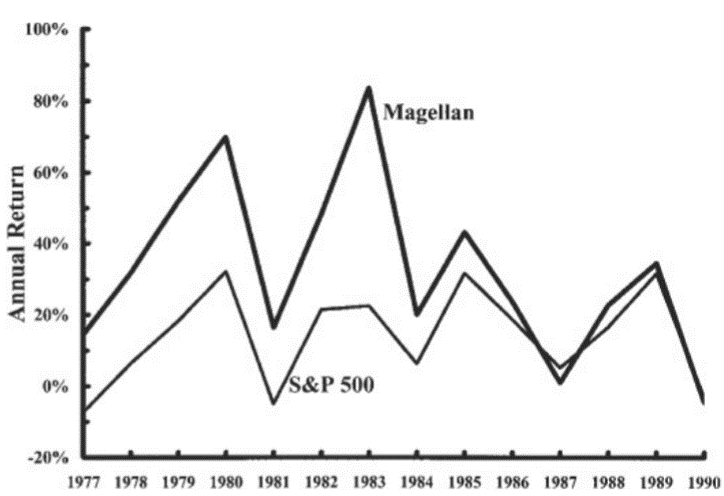

The biggest example being the Magellan fund, which was managed by the then star fund manager Peter Lynch from 1977 to 1990. "The fund delivered excellent returns at 29% CAGR in the 1980s compared to S&P's 15% CAGR. However, as the fund size kept growing, the returns kept shrinking and ultimately Lynch quit the industry in 1990," Shyamsunder said.

The data and the example show that though a skilled fund manager can outperform the market, there is little chance that they can do so year after year.