Listen to this article

In a major restructuring, IRDAI will soon bring uniformity in the commission payment of agents and intermediaries across life, general and health policies.

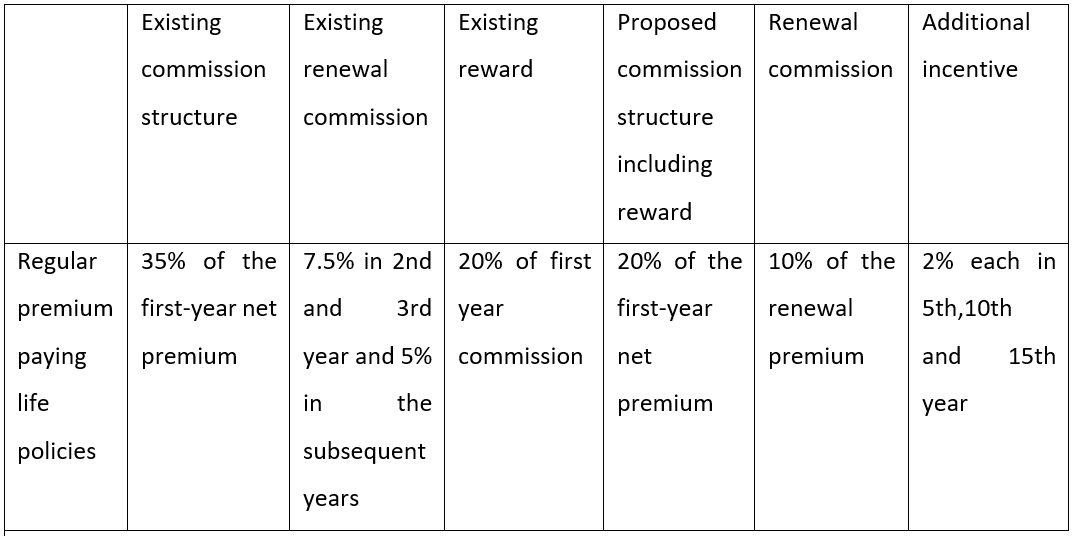

IRDAI has issued draft guidelines on the payment of commission and reward to insurance agents in which it has proposed to reduce first year commission of life insurance agents on regular premium paying policies from 35% of the net premium payment to 20% of the net premium payment including rewards.

However, the insurance regulator has proposed to increase renewal premium to 10% in the subsequent years instead of 7.5% in the second and third year and 5% in the subsequent years.

Another interesting move is introduction of longevity incentive i.e. additional commission will be given to life agents and intermediaries if their clients remain insured for 5, 10 and 15 years.

Here are other key highlights of the draft regulations:

- If the annual expense of management does not exceed 70% of the total allowable limits, the insurers can also offer commission in accordance with the board approval

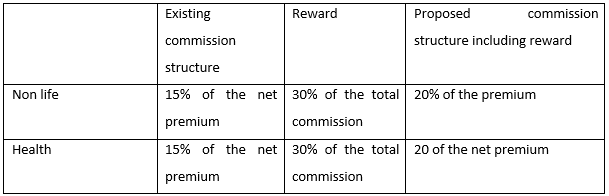

- Maximum commission in general and health policies will be 20% including rewards

- In addition, life insurers can also pay additional commission of 2% of the total premiums paid each time at the end of 5th, 10th and 15th year

- Commission on single premium life policies remains intact at 2%

- For group fund policies i.e. annuity policies, the commission is capped at 0.5%

- Just like direct plans in mutual funds, insurers can offer policies directly to costumer with discounts

- Insurers will have to make a written policy for payment of commission or reward to insurance agents and get it approved by its board. The board has to review such policies annually

- Insurers may offer additional rewards to agents and intermediaries based on their performance

- Performance of insurance agents should be evaluated based on their contribution towards increasing insurance penetration and density, if they work in the interest of policyholders, if they comply with regulatory norms and commensurate with business strategy of the insurer, their efforts to bring down cost to conduct business and simplify systems and so on

- This new commission structure, if implemented, will be applicable for a period of 3 years from the date of implementation

Proposed commission structure on regular premium life policies like term, whole life, money back and endowment policies:

Proposed commission structure on non-life and health policies