Listen to this article

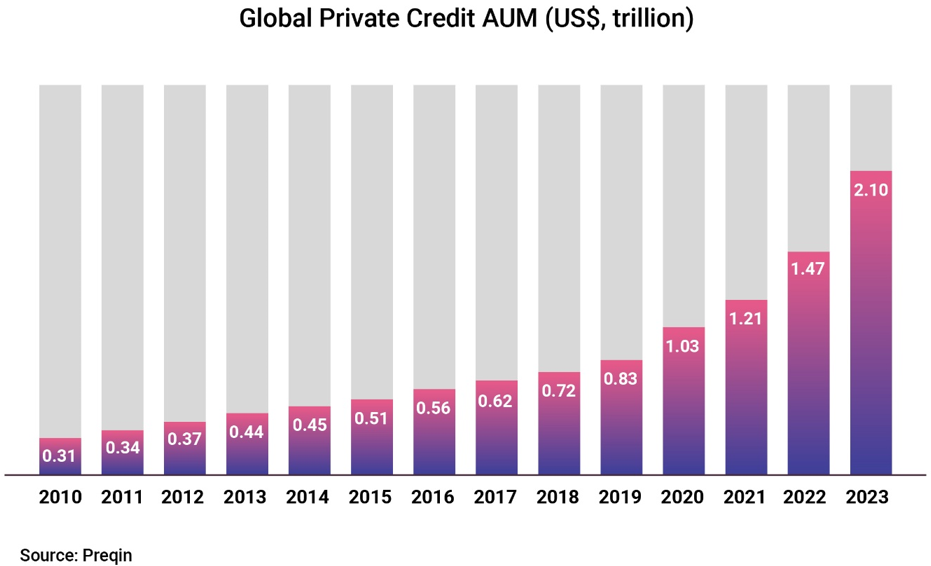

In India, the rapid growth in the economy led to a growth spurt in mid-sized businesses that are increasingly seeking tailored financial solutions that private credit can only provide with flexible structures. As per Preqin, the provider of alternative assets data, tools and insights, the AUM of India-focused private debt skyrocketed over 25x from US$0.7 billion in 2010 to US$17.8 billion in 2023. With this, it surpassed the growth witnessed by other asset classes in India such as Venture Capital (8x), Private Equity (2.1x), Real Estate (1.6x), and Infrastructure (1.8x) over the same period. This also made India the APAC leader in the Private Credit market.

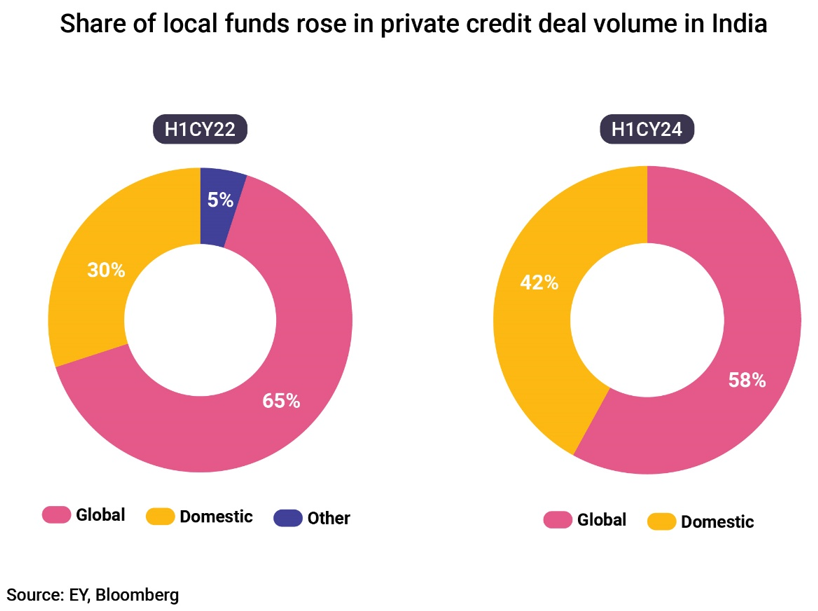

With respect to the market share in the private credit space, there has been a trend reversal in the last few years. Domestic private credit funds started stealing the pie from global counterparts due to several factors such as the local expertise of asset managers and other factors as outlined below helping them to achieve market depth and diversification.

The nature of private credit investments

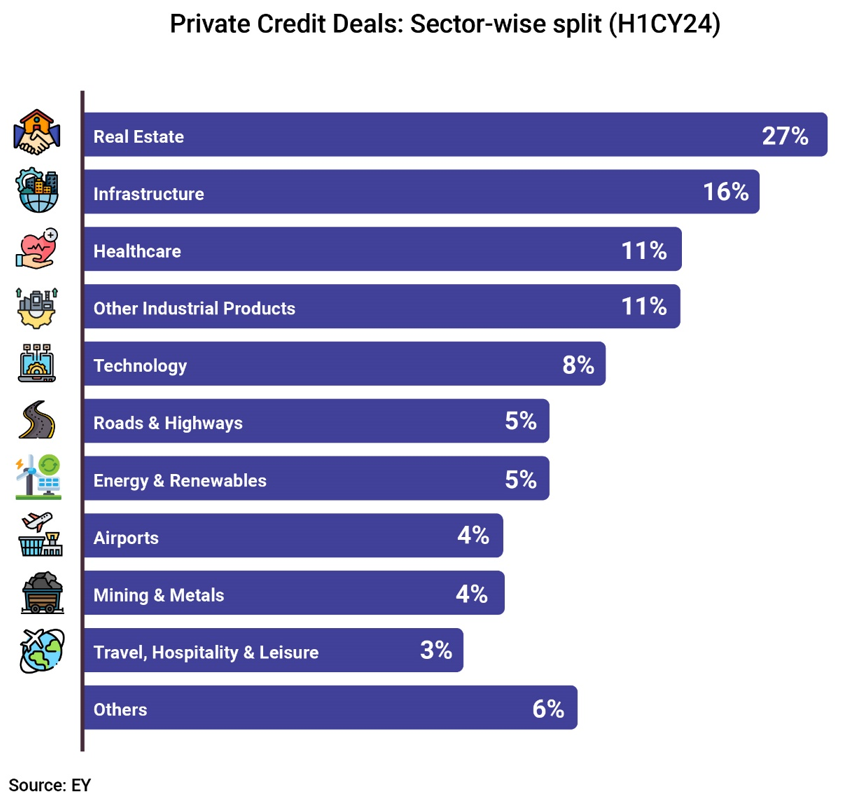

In the first half of 2024, India’s private credit market gained significant momentum as private credit investments surged to an all-time high for any six-month period. Investments totaled US$6 billion which are deployed across 96 deals. Like before, real estate dominated the space, in terms of value, followed by infrastructure, and other sectors.

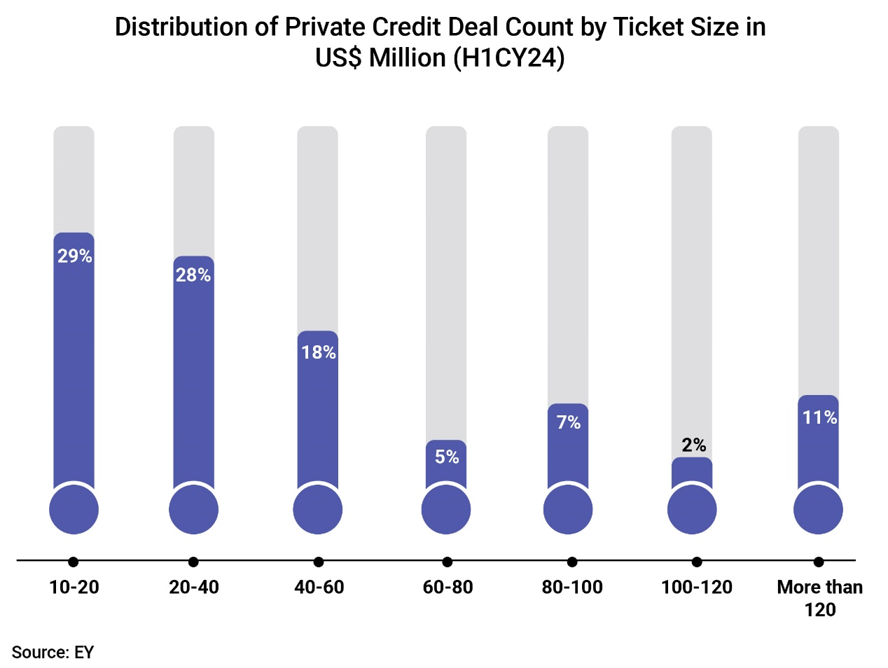

However, the average deal volume in India shrank in H1CY24 compared to 2023, which could be somewhat attributed to the growth in mid-market enterprises. The average deal volume in the period stood at ~US$25 million compared to ~US$161 million across the rest of Asia (Preqin). As depicted in the chart below, private credit deals in the range of US$10 million to US$40 million accounted for more than 50% of all private credit transactions in H1CY24.

- Infrastructure spending: Private credit gets an impetus from the government’s push for large infrastructure projects. The Centre has doubled the spending on infrastructure projects over the past three years with the objective of boosting the economy. In the Union Budget, a record INR 11.11 lakh crore has been earmarked for such projects in the financial year ending March 2025 (FY25), which in terms of GDP, stands at 3.4%. As large corporations win more and more infrastructure projects, ancillary work is being awarded to more and more small and mid-sized companies boosting the demand for private credit.

- Flexible financing solutions: The private credit players are able to provide flexible financing solutions to fast-growing mid-sized companies, including favorable loan structures and repayment schedules, compared to traditional bank loans, while catering to borrowers’ specific needs.

- Regulatory climate: The enactment of the Insolvency and Bankruptcy Code (IBC), 2016, acted as a catalyst for the growth of the private credit market in India. It became a statutory instrument to effectively safeguard funds’ interest in debt investments in companies that are moved to IBC proceedings and boosted investors’ confidence. This is because IBS helped in expedite insolvency resolutions and maximize returns for creditors.

- Role of digital infrastructure: India’s digital infrastructure (with the likes of the Account Aggregator framework) has been playing a key role in developing the private credit market by streamlining the underwriting process. It made easier for private credit lenders to access goods and services tax (GST) records, credit histories, and other relevant information.

- Tax reforms: Private credit funds, mainly Debt AIFs, got the much-awaited level-playing field in the taxation of debt investment products as the Finance Act 2023 brought tax parity across all debt products. It leveled the playing field for debt asset managers of various pooled investment vehicles by standardizing taxation.

- Shift in investors’ preference: Higher disposable income and better access to financial information have enabled the young Indian population to make prudent investment decisions, increasingly moving them away from traditional investment avenues to private credit funds/AIFs.