Listen to this article

Debt plays a major role in the economic growth of a country as it offers a non-dilutive, lower cost alternative to companies looking to raise capital. The primary sources of debt are banks, NBFCs and the public corporate bond market.

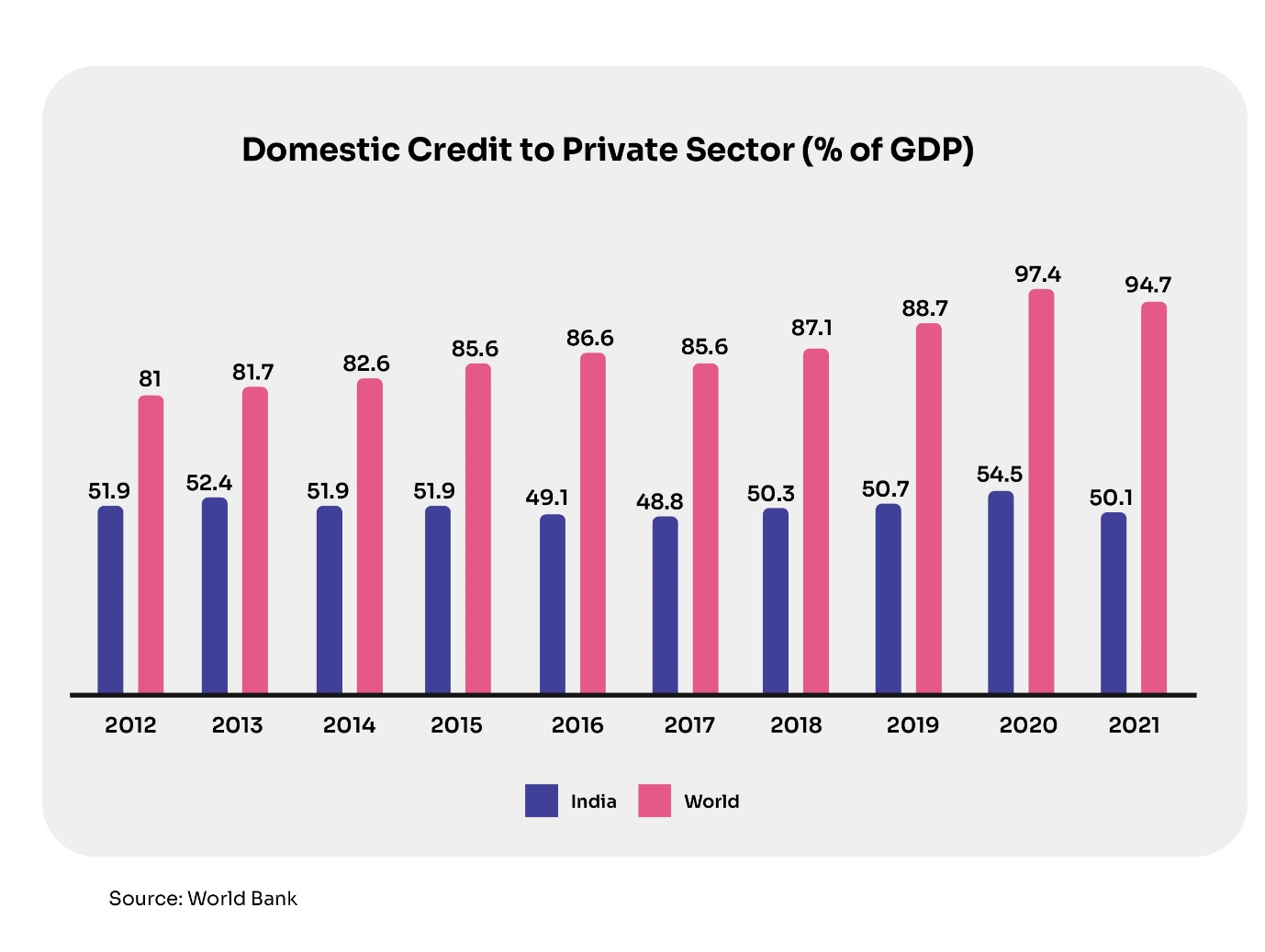

Despite being the fastest-growing economy in the world, India still faces significant gaps in enterprise credit which cannot be serviced by traditional sources of capital. This is indicated by the fact that India’s domestic credit to the private sector has hovered around 50% of GDP compared to a consistently higher and steadily increasing world average of 95%. This indicates a significant room for growth in debt in relation to the size of the Indian economy.

The mid-market enterprises (MMEs) in India are the pillars of growth. There are 15,000+ companies in the ecosystem contributing over 40% to India’s GDP, employing 40% of the country's workforce and generating nearly 50% of its exports. However, majority of these companies have little or no access to the debt market.

Roadblocks to growth

Traditional lenders such as banks and larger NBFCs are inflexible in enterprise lending and tend to serve the most vanilla needs through policy-based lending. On the other hand, mutual funds and insurance companies are restricted by their respective regulations and face lack of access to this space and limited ability to assess credit worthiness.

Most of these entities rarely have the expertise to navigate public capital markets, further exacerbated by the perils of asymmetrical information and smaller ticket sizes, which may not garner investor interest.

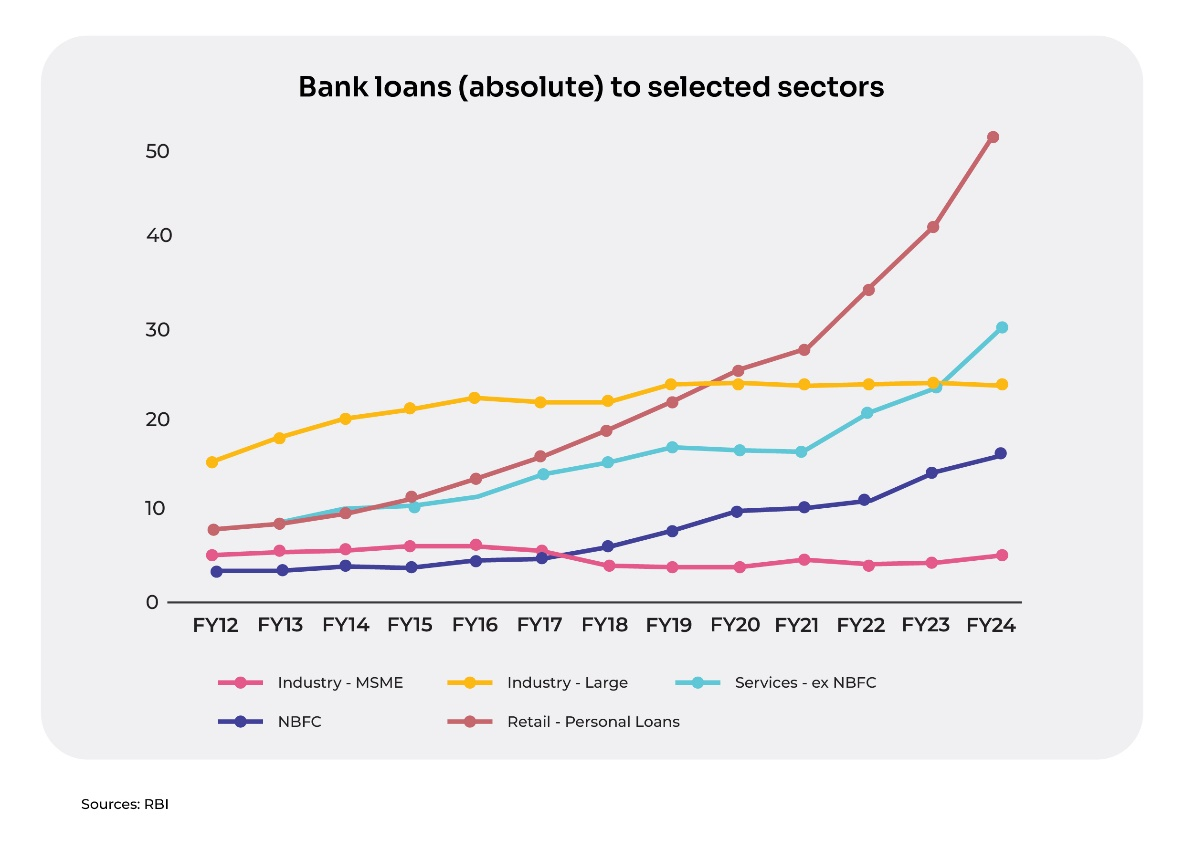

Banks and NBFCs have largely pivoted towards retail lending with loans to industry growing at a slower pace than average disbursements. In the past 12 years, retail loans by banks clocked a CAGR of 16% while banking credit as a whole rose 10%. In the same period, bank lending to large businesses and MSMEs has relatively stagnated with a CAGR of 3% for each, respectively.

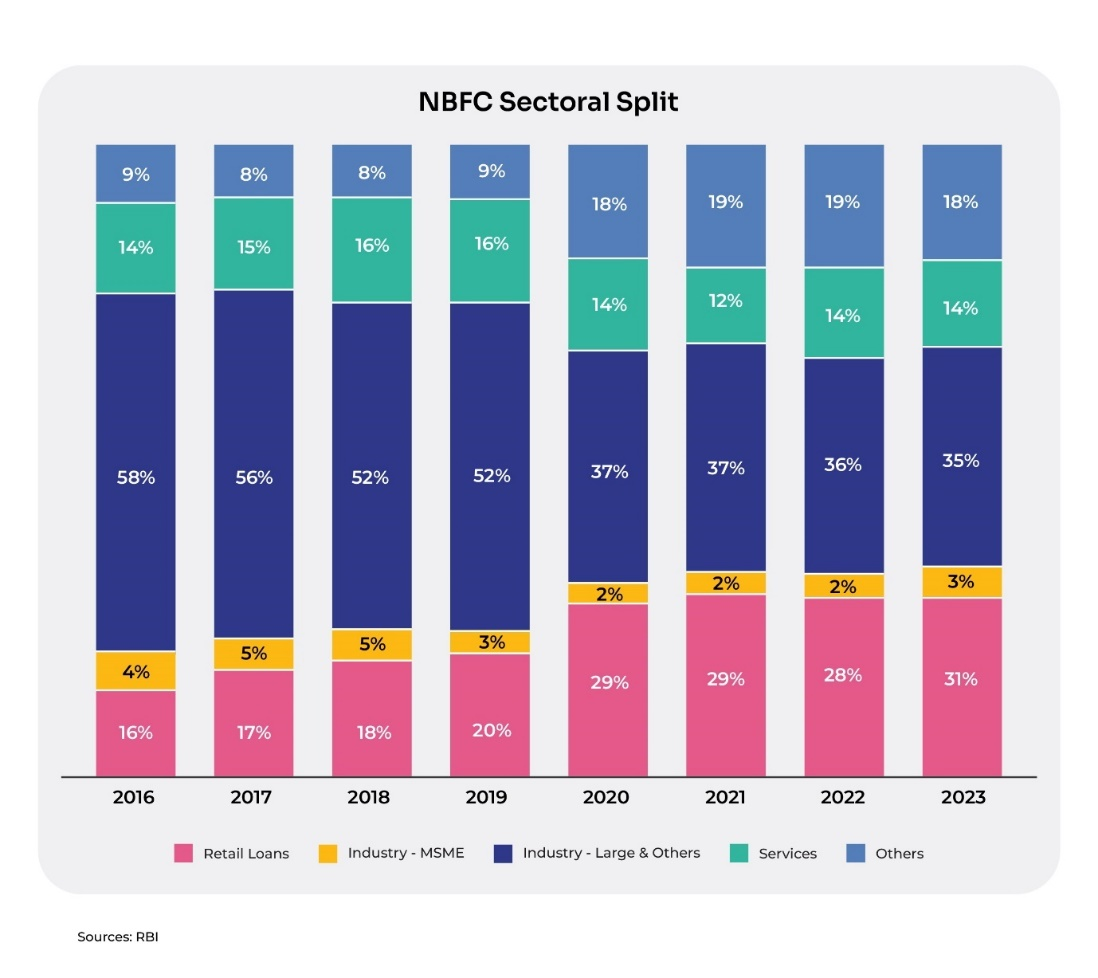

NBFCs depicted a similar trend in the last 8 years with retail lending recording a CAGR of 23% while their gross advances increased by 11%. In contrast, NBFC lending to large and other businesses clocked a CAGR of 6% and 8% for MSME in the same period.

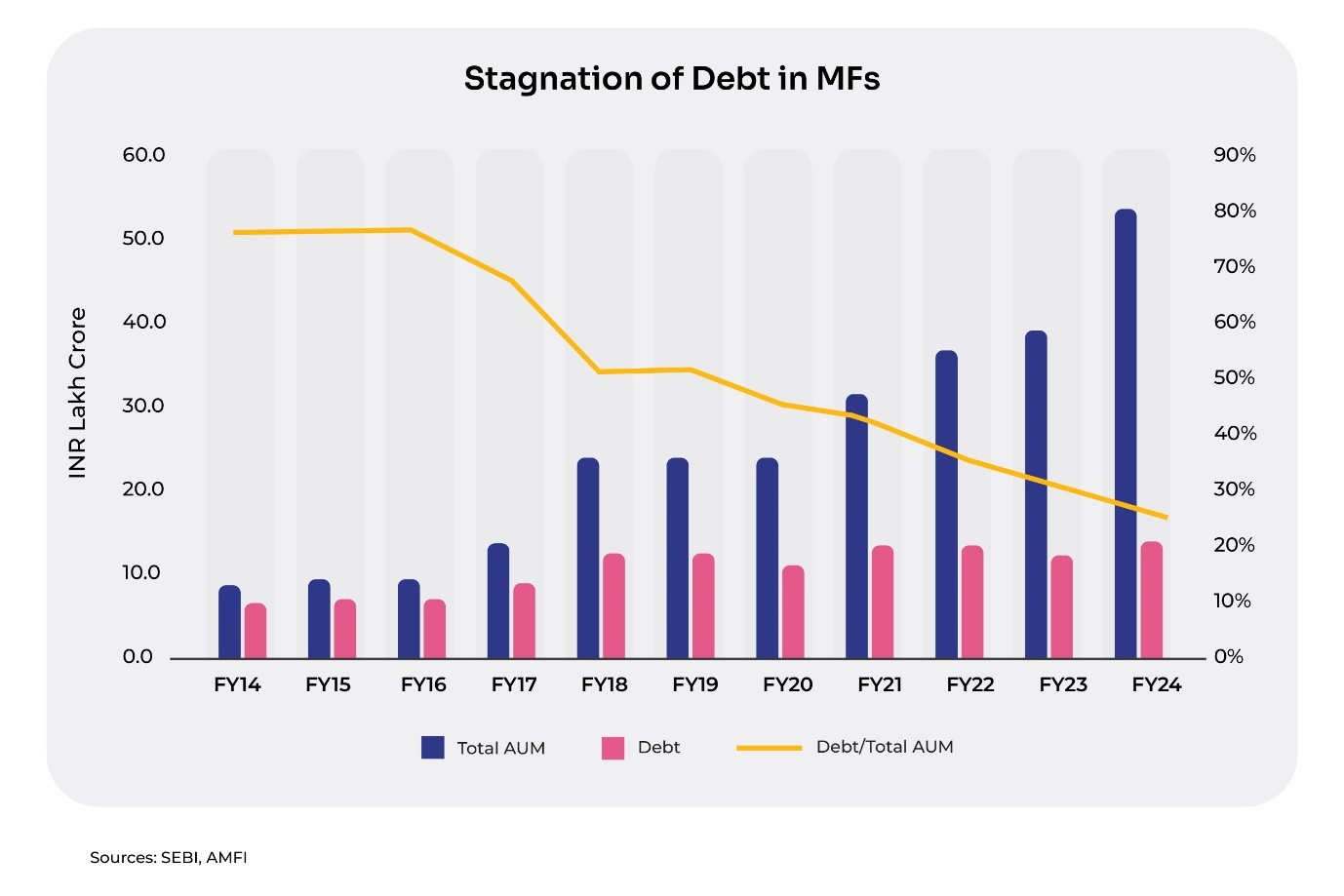

Over the last 10 years, debt mutual funds in general have seen a stagnation in AUM. As a percent of the total AUM, debt mutual fund AUM slipped from 75% in FY14 to 25% in FY24.

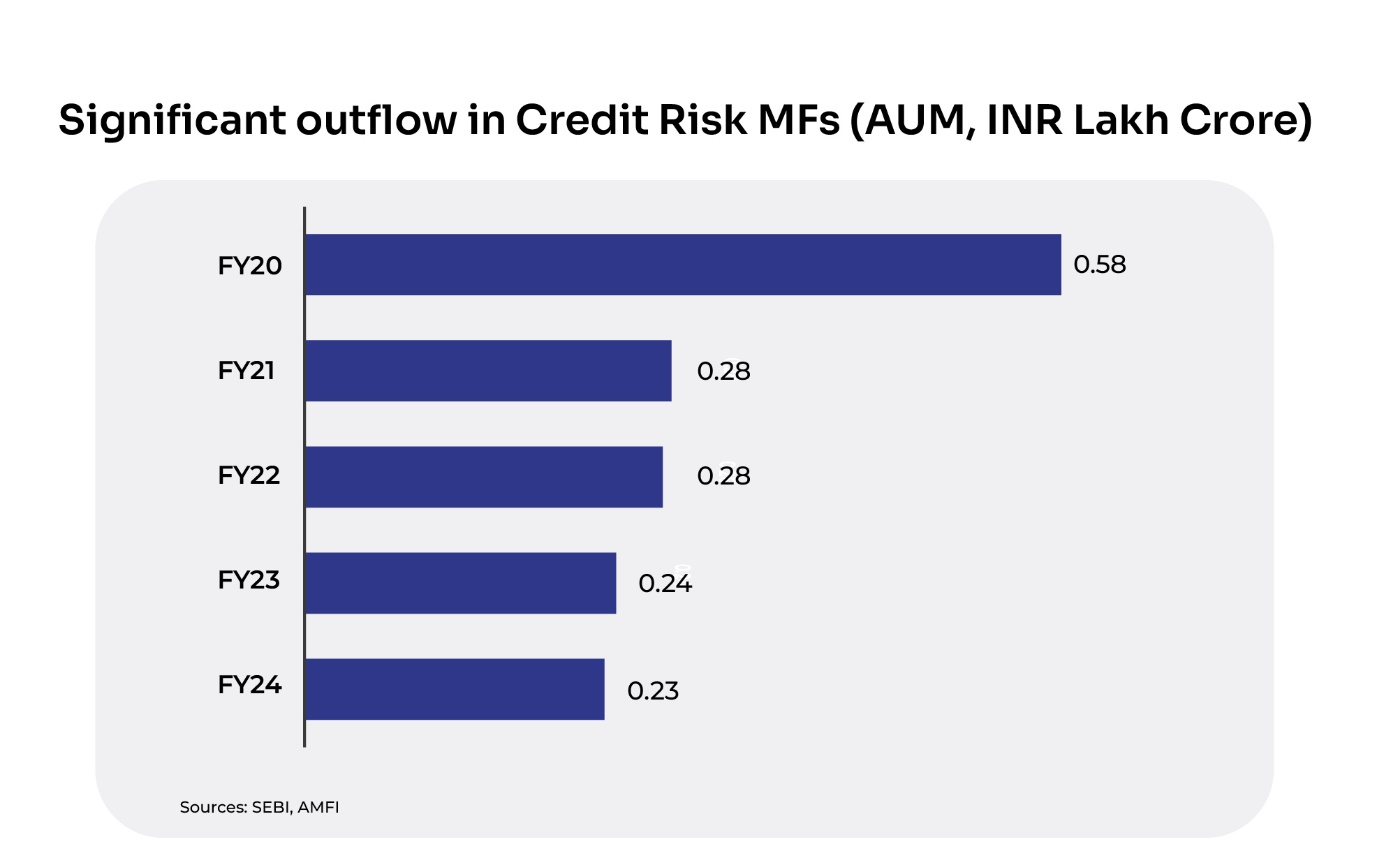

On the other hand, credit risk mutual funds have witnessed significant outflows with their volume degrowing by 2.5x in FY24 compared with FY20.

The domestic bond market has not been able to alleviate the situation. The overall market is dominated by government securities (G-Secs) and State Development Loans (SDL bonds), which accounted for 70% of the total outstanding in the bond market, while corporate bonds accounted for 22% of the same as of March 2024. In terms of share in GDP, the corporate bond market accounts for 16% (2021), which remains sub-optimal compared to its Asian peers like South Korea (87%), Malaysia (57%), and China (36%).

In such a scenario, what can plug the significant gap in enterprise credit, mainly the mid-market enterprises that hold the potential for the next leg of growth in India?

The emergence of private credit

Private credit provides an alternative source of financing for businesses with unique funding needs and irregular cash flows, cases which banks may avoid due to inflexible policies and regulatory restrictions. Private credit lending takes place mostly via funds/investment vehicles handled by specialized asset managers. In such funds, money is raised from sophisticated investors which are then deployed to entities as per covenants that suit the risk-return spectrum of the vehicle. The tasks related to origination, due diligence, monitoring and recovery (if required) are handled by the fund. With this, investors get access to a professionally managed portfolio consisting of 10-20 entities.

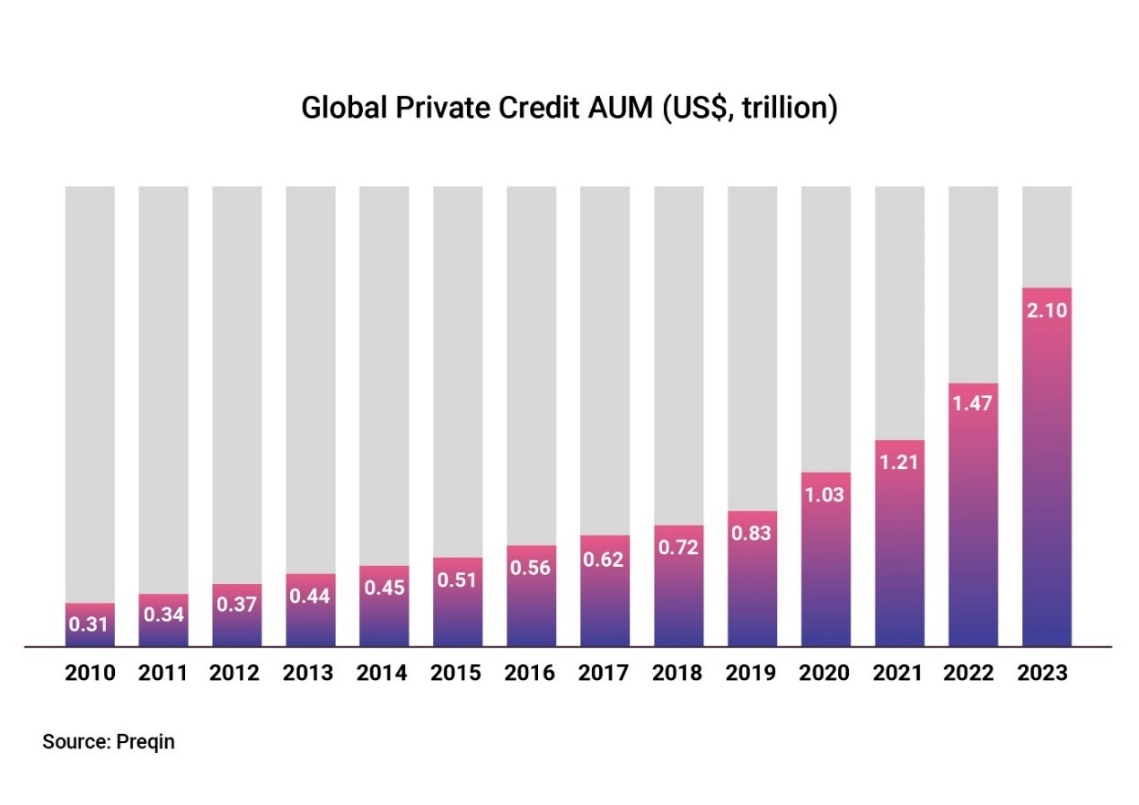

The Private Credit market has been growing at a fast pace across the world and India is no exception. It witnessed a 5x growth in assets under management (AUM) over the last 10 years to over US$2 trillion in 2023.

Globally, the market started gaining pace as banks retreated from lending to small and mid-sized businesses and to companies backed by Private Equity. On the other hand, mid-market corporates are turning towards private credit funds seeking tailored financial solutions that such vehicles can provide with flexible structures.

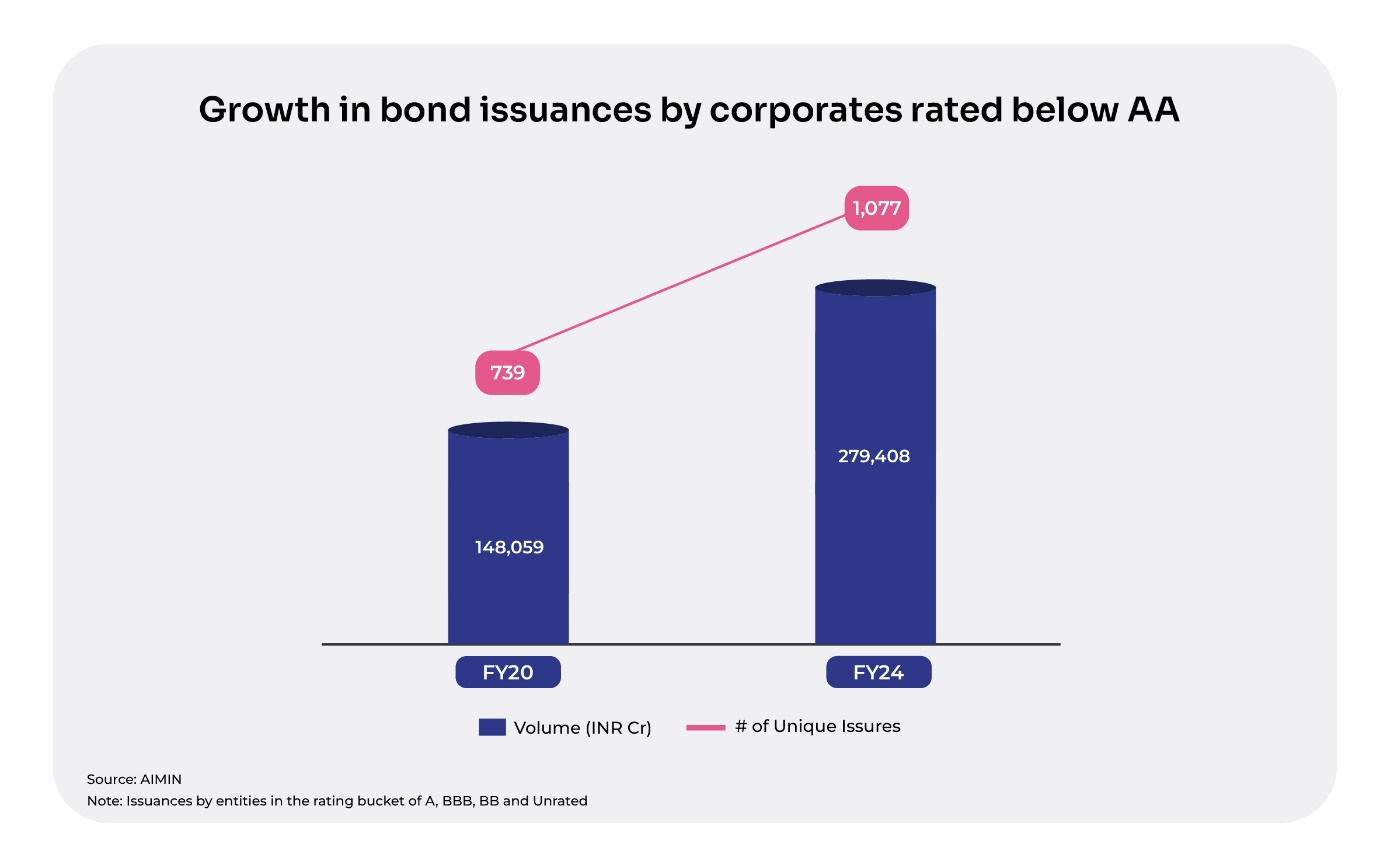

Although India’s corporate bond market has been dominated by issuances in the higher credit rating categories, lower rated entities have been tapping the bond market increasingly. It is attributed to factors such as faster TAT compared to banks, flexible end-uses and security structures, emergence of online platforms and the emergence of specialized private credit managers in the performing credit space, which cater to mid-sized, EBITDA positive and cash flow generating companies with end uses of growth capital, capex, mezzanine financing and acquisition (ticket size of loans Rs.50-300 crore).

The entities in the performing credit space, to which banks generally offer term loans, are able to issue debentures into which funds invest. Often, and especially for corporates, an issuance for a fund may be the entity’s maiden capital market issuance and rating exercise. The fund may also be able to provide guidance in navigating the nuances of capital market issuance.

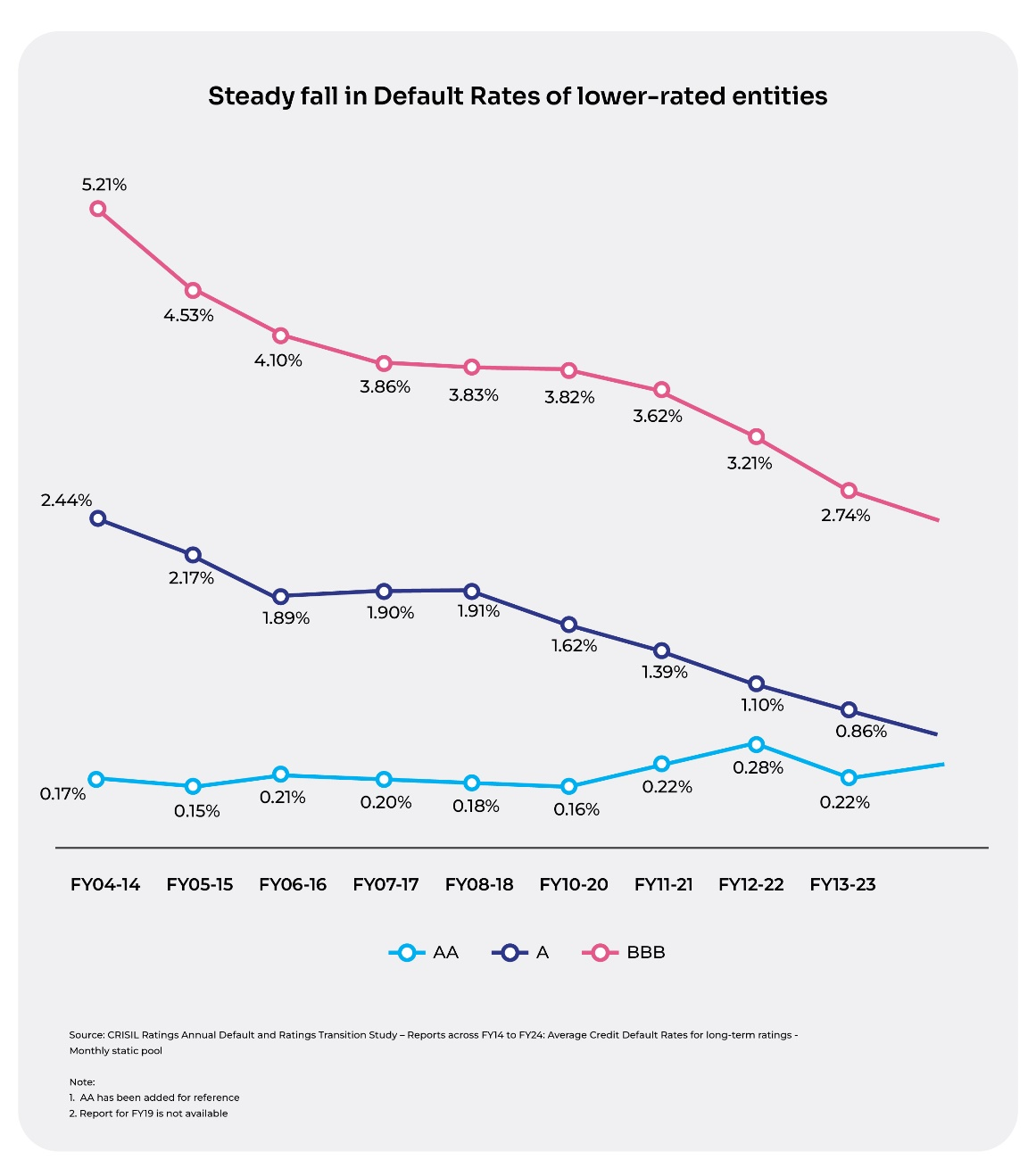

Lower rated entities (below AA) are deemed to be riskier compared to the above AA rated category due to their higher default rates. However, recent studies have shown default rates of entities in the space have been declining steadily due to factors such as:

- Enactment of the Insolvency and Bankruptcy Code that has imparted credit discipline among such corporates

- Improved scale and profitability of the entities due to the growth and digital advancement of the Indian economy

- Industry-wide consolidation

- Lower volatility in operating parameters

What’s in it for investors?

In the public debt market, it has become difficult for investors to generate real returns. However, it makes sense to cautiously move into the private credit market given the immense potential in the space to earn superior returns. Recent regulatory steps like the enactment of the Insolvency and bankruptcy code and the introduction of the account aggregator framework brought confidence in the market and enabled transparency and scope for efficient decision-making about borrowing entities.

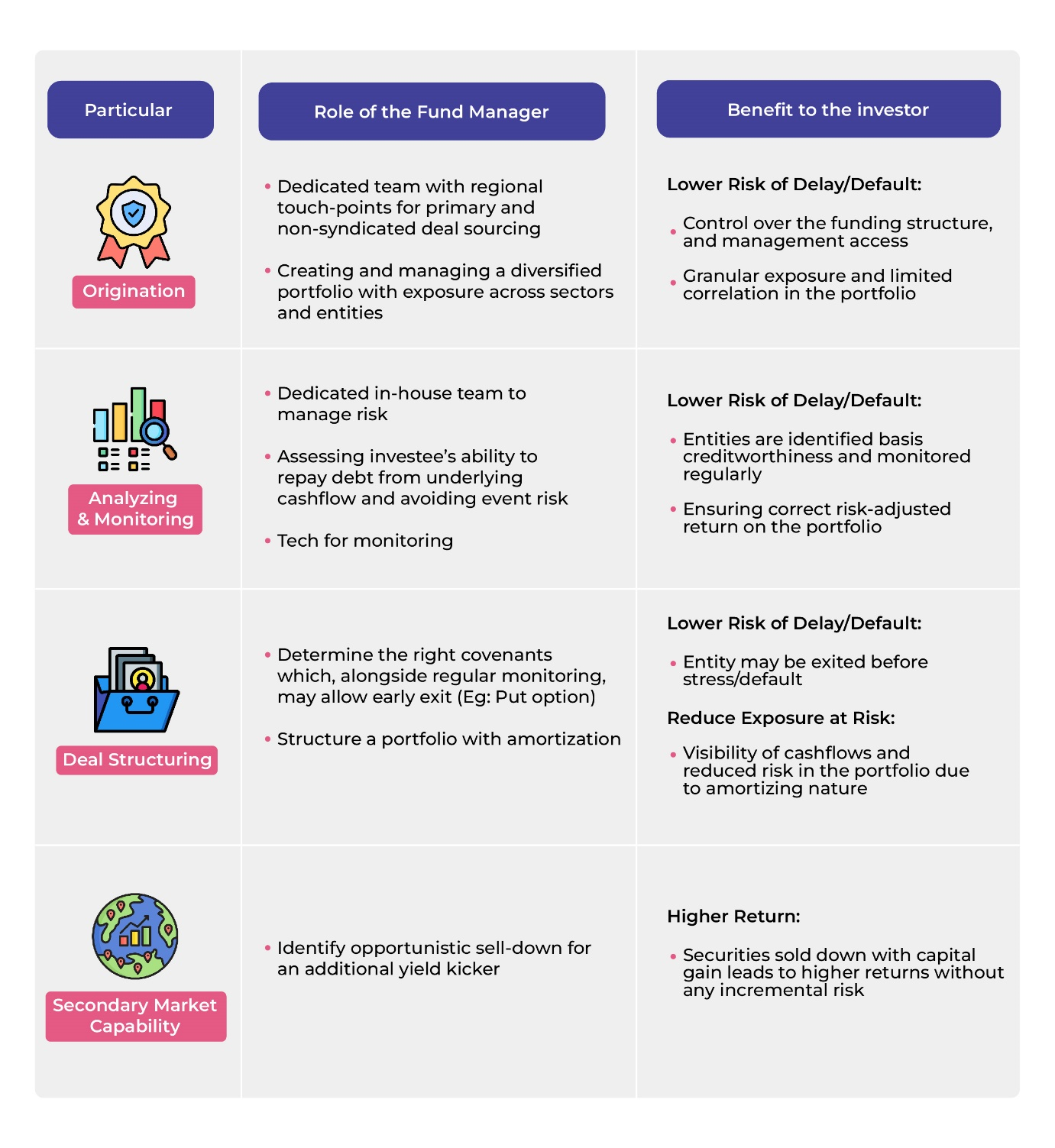

Further, choosing a highly professional fund manager is extremely useful while investing in the space as such risks can be mitigated ensuring stability and predictability of returns. Below are the factors investors should consider before investing in private credit funds:

Disclaimer:

The information provided in this article is for general informational purposes only and is not an investment, financial, legal or tax advice. While every effort has been made to ensure the accuracy and reliability of the content, the author or publisher does not guarantee the completeness, accuracy, or timeliness of the information. Readers are advised to verify any information before making decisions based on it. The opinions expressed are solely those of the author and do not necessarily reflect the views or opinions of any organization or entity mentioned.