One of the most popular (and probably an ice breaker) question I get as an Investment Manager is – What’s your take on market? or “market kya lagta hai?”. I have always answered it in two parts - my view on macro economy and market valuations. Since macroeconomics is not the discussion topic of this article, we shall focus on the second factor – market valuations.

Typically, the answer to market valuation is guided by where was the index price earnings (PE) multiple in relation to its historical average. If current market PE is higher than historical average, market is supposed to be expensive and vice-versa.

Nifty 50 Index trailing twelve month (TTM) PE as on September 30, 2021 is at 28.3x, which is at 52% premium to its 20-year monthly average based on data provided by Bloomberg.

However, this is an inconsistent way of looking at market valuations. At Union Mutual Fund, we have identified the Fallacy of using the Index PE Multiple as a benchmark for valuation.

Before we start our discussion, an important note – the index providers are accurate in the way they calculate the Index Earnings Per Share (EPS) or Price Earnings (PE) multiple. In this note we are highlighting the fallacy in its interpretation as a fair valuation benchmark by investors.

Mystery coin box experiment

Let’s understand the inconsistency of this conventional logic using a simple example.

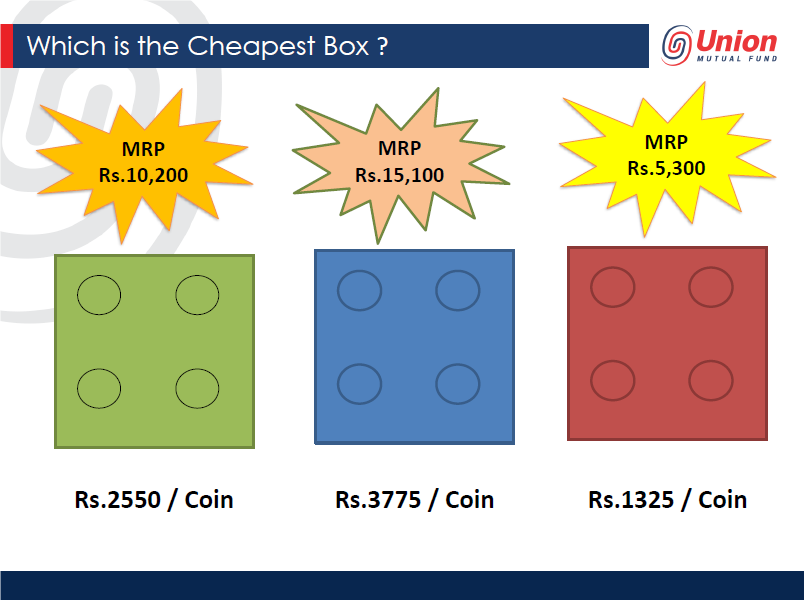

Suppose there are three coin boxes (Green, Blue and Red) containing 4 coins each. These can be either gold coins or silver coins.

We have to judge the value of each of these coin boxes, first without looking at what is inside the box and then after looking at what is inside.

What we know is that the value of one gold coin is Rs.5000 and one silver coin is Rs.100.

First we try to judge the Value of these boxes ‘without looking what is inside’:

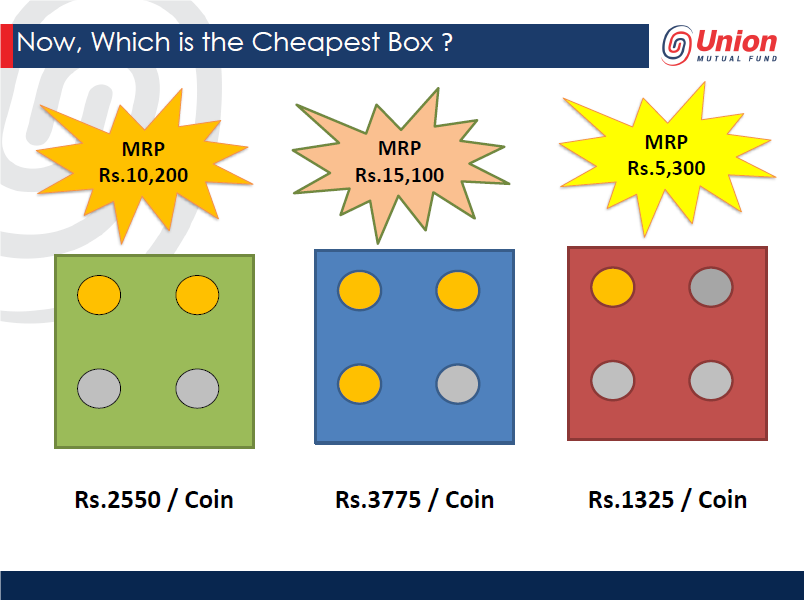

Based on the above data, we may deduce that the Red Box is the cheapest, as its available for just Rs.5,300 or for Rs.1,325 per coin and vice versa for the Blue Box.

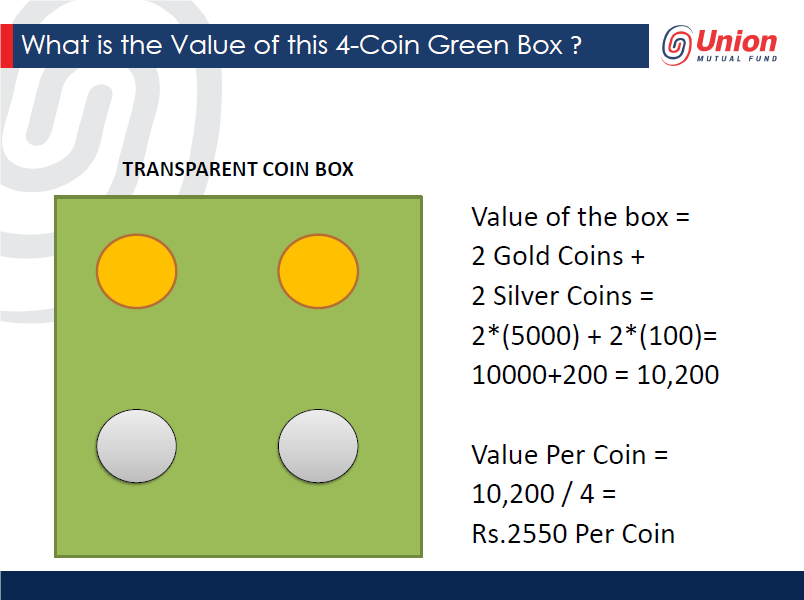

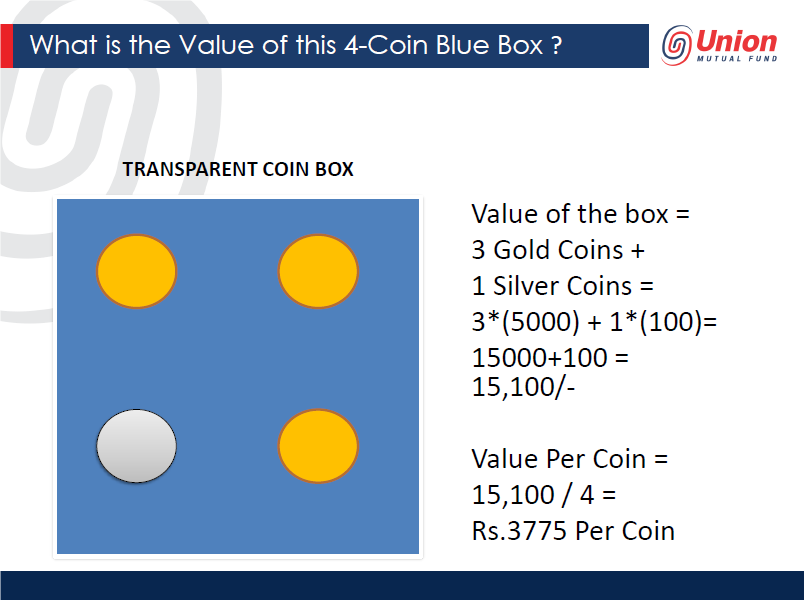

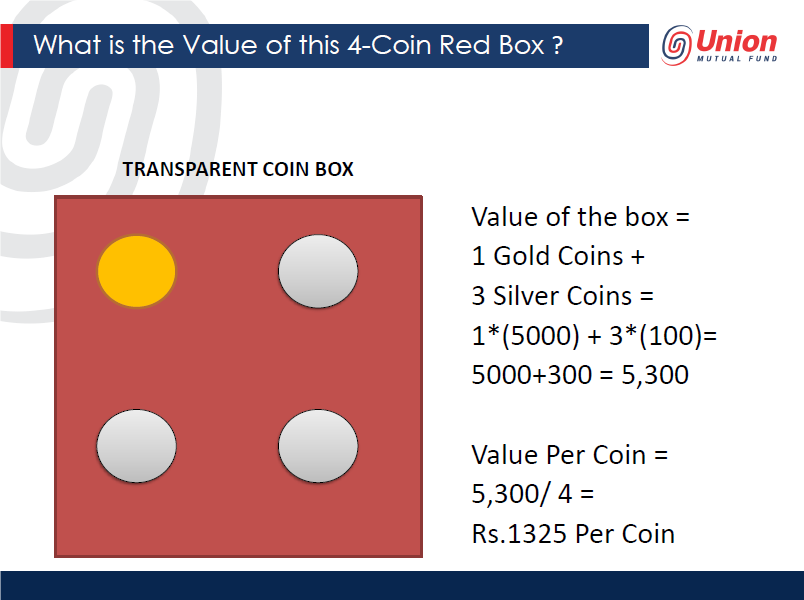

Now let’s look at what is inside these boxes:

Now let’s again judge, which is the cheapest box.

Since you know what is inside the box, you can make a fair assessment of the Fair Value of each box. Fair Value of each box is the sum total of value of each coin present in the box. Based on this assessment, we can see that all the boxes are fairly priced.

Mystery coin box and stock markets

We shall now extend this metaphor to stock markets. The mystery coin box is like a stock market index (e.g., Nifty 50 Index, BSE Sensex, etc.) and the coins represent individual stocks. Gold coin represents High P/E stocks in sectors like FMCG, IT, telecom, etc., while silver coin represents Low P/E stocks in sectors like banks or metals.

Thus, you can now visualize, how you can make incorrect judgements by just looking at index P/E (or Price/Book or Dividend Yield or similar index-based valuation measures). For example, if the index components in 2012 had higher number of stocks commanding low P/E (like the silver coin) then the Index would appear cheaper (like the Red Box). However, if the index in 2021 has a higher number of stocks commanding high P/E (like the gold coin) then the Index would appear expensive (like the Blue Box).

According to us, the best way to judge the value of any index is to judge the Fair Value of each stock (like the coins in the box) and then aggregate the Fair Values of all the stocks in the index, to arrive and the Fair Value of the Index.

Conclusion:

Investors should not depend on index PE multiples to make judgements about overall market valuations. India’s market over the last decade appears to have turned expensive based on PE multiples as companies which deserve to trade at high multiples have delivered superior earnings growth, compared to most cyclical companies, which deserve to trade at lower multiples. Also, the reported PE multiples of the index has been distorted due to sum of the parts valuation for some of the large index weights.

According to our research, the Fair Value approach is directionally correct and consistent approach to make judgements on market valuation.

Disclaimer: The views, facts and figures in this document are as of 20th October 2021, unless stated otherwise.

The above information alone is not sufficient and should not be used for the development or implementation of an investment strategy. The recipients of this material should rely on their investigations and take their own professional advice. The Sponsors/ the AMC/ the Trustee Company/ their associates/ any person connected with it, do not accept any liability arising from the use of this information and disclaim all liabilities, losses and damages arising out of the use of this information.

Vinay Paharia is the Chief Investment Officer of Union Mutual Fund. The views expressed in this article are solely of the author and do not necessarily reflect the views of Cafemutual.