In the ongoing active vs passive debate, there has been lots of discussion around the ability of active funds to beat their benchmark index. Unlike their passive counterparts, active funds invest in stocks that are different from their benchmark and invest in varying proportions. As these funds strive to beat the benchmark, they involve active risk.

Some believe active funds fail to surpass their benchmark and do not justify fund management fees. While there is another set of investors who hold positive views.

What could be the reason behind these contradictory views? Union MF in its latest report decodes the difference backed with some solid data.

Underperforming active mutual funds (Single-date analysis)

There are more than 250 trading days in a typical year; however, certain investors look at funds' performance as on a single date rather than the performance across timeframes. As a result of which the analysis only accounts for less than 0.4% of the total possible outcomes.

Here is how this can be understood better.

As seen, most of the schemes have underperformed over different periods as on 30 Sep 21.

Such ‘single-date’ analysis fail to demonstrate funds’ performance throughout the previous years. Further, they may also be impacted by abnormal events like the market crash in Mar 2020 due to covid-19.

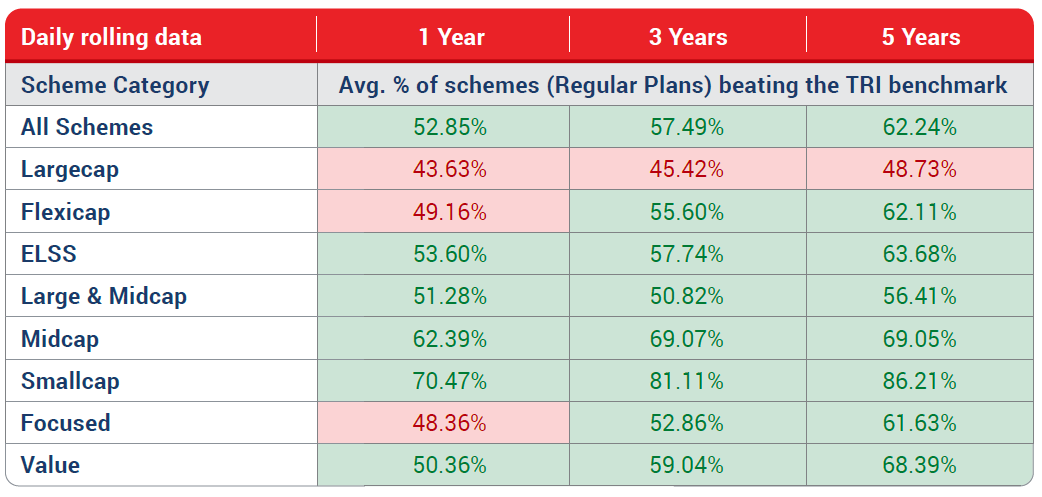

Over performing active mutual funds (Daily rolling basis)

Analysing performance on a daily rolling basis gives a more meaningful insight. Daily rolling basis means calculating returns for the period ending 1st Jan 12, then 2nd Jan 12, thereafter 3rd Jan 12, and so on. Then we see how many funds in that category have outperformed the relevant benchmark on each date. An average is taken across time periods to ascertain outperformance in a category.

Let’s illustrate this numerically.

As observed, apart from the large cap category, majority of the schemes have surpassed their benchmarks. Notably, the extent of outperformance is higher over longer periods.

Shortcomings of the study

Like most studies, the study conducted by Union MF is also subject to certain shortcomings which are common to both methods.

Survivorship bias: Re-categorization changes in 2018, lead to a merger of many schemes into extant schemes. The study does not account for the performance of these merged schemes.

Style shift due to re-categorization: Certain schemes have changed their strategy as per the new categorization standards, which means their past performance was achieved through strategies that might be different from existing strategies.

Conclusion

Prevalent ‘single date’ performance analysis indicates that active funds do not outperform benchmarks. However, the study ignores the performance throughout the year and is easily biased by abnormal events, and does not give complete & reliable insights.

The above limitations can be eliminated through rolling return analysis which provides a more reliable insight in appraising fund performance. Such analysis reveals that on average active funds in India have outperformed their respective benchmarks.

Vinay Paharia is the Chief Investment Officer of Union Mutual Fund. The views expressed in this article are solely of the author and do not necessarily reflect the views of Cafemutual.