Listen to this article

Debt market has off lately caught attention due to central banks across the globe tightening the rope of liquidity.

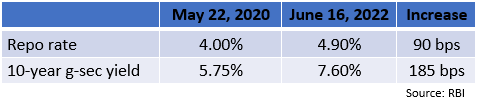

With RBI stepping into rate hike mode, bond yields have suddenly caught momentum. India’s 10-year g-sec yield rallied since the breakout of the pandemic from 6% in July 2020 to 7.6% as on June 13, 2022 (Source: Bloomberg). This may have brought the debt market into the spotlight.

If experts were to be believed, current bond yields may have factored in a large part of the future expected rate hikes. To understand this in-depth, we analysed historic data. The analysis revealed that interest rates are a lag indicator while bond yields are a leading indicator.

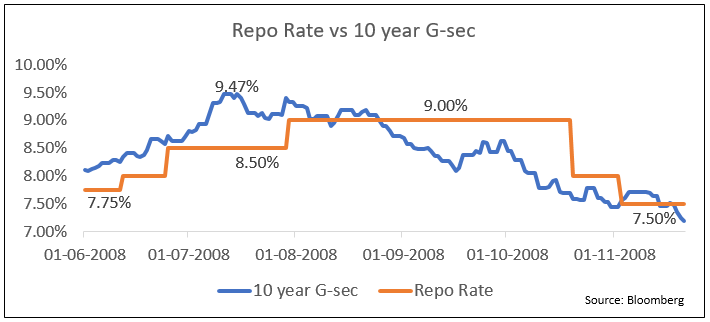

Bond yields are forward looking by nature. As evident from the above chart, 10-year g-sec touched its high in mid-July 2008 before the repo rates peaked in August 2008. Subsequently, yields started correcting in September 2008 well in advance before the repo rates came down. This phenomenon is seen in almost all the rate action periods. This might be the case today as well where repo rates have risen by 90 bps (basis points) while bond yields have risen disproportionately by 175 bps.

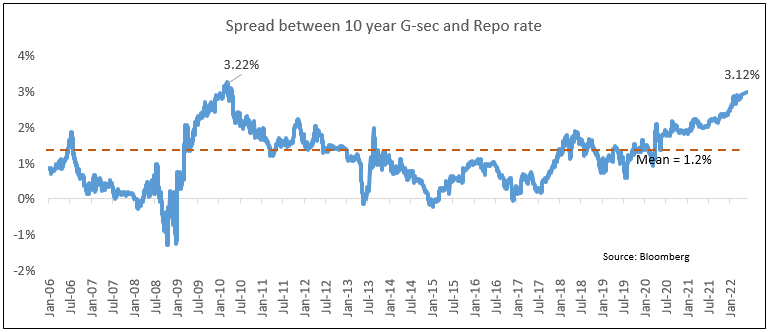

G-sec spread over repo – A crucial indicator

Interestingly the spread between the repo rate and interest rate may give us a directional indication. We did another analysis to look at the spread between g-sec yield and repo rate.

It has been observed that sooner or later, the spread corrects and comes closer to its mean of 1.2%. Presently, the spread at 3.12% is close to its all-time high of 3.22% clocked during GFC (global financial crisis). Thus, it may be construed that we may have entered the fag end of the upward sloping yield curve and the yield correction might be around the corner. Investors may keep a close watch on the levels.

What should investors do?

Our analysis has led us to believe that this may be the right time to invest in long duration funds. Investing in such funds may help you lock your funds at reasonably attractive levels and may also offer you an opportunity to ride the bond market rally, should yields correct from here.

In 2021, LIC Mutual Fund was proactive in identifying the rate hikes well in advance and we brought down the duration of our long duration funds to minimum thereby safeguarding investors’ wealth in a rising interest rate scenario. We have now started increasing our durations to take advantage of the potential yield corrections. We expect another 75 bps rate hike by December 2022. However, we also believe the same may have been factored in the current bond yield pricing, making current levels an attractive level to invest.

Nityanand Prabhu is Executive Director & Business Head of LIC Mutual Fund

Disclaimer: This disclaimer informs readers that the views, thoughts, and opinions expressed in the article belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.