The proceeds from ULIPs, which used to be completely tax free, were made taxable from February 1, 2021. The income tax department has now come out with details as to how the taxation will take place when an investor holds multiple ULIPs.

How are ULIPs taxed?

On February 1, 2021, the government withdrew tax exemptions given to ULIP investors in cases where the yearly premium exceeds Rs. 2.5 lakh. This means that proceeds from any ULIP investment started on or after February 1, 2021 with annual premium of over Rs. 2.5 lakh will face capital gains tax.

What happens when an investor has multiple ULIP investments?

To determine the maximum exemption an investor can claim, one needs to first divide the policies into two sections — old (policies bought before February 2021), a combination of old and new policies (policies that bought before and after February 2021) and new (policies bought after February 2021).

Since the new rules came into force from February 1, 2021, all policies bought before this date are exempt from paying any capital gains tax.

Coming to other scenarios, investors have the option to claim one exemption (for either just one policy or on an aggregate basis).

Let's understand the above condition with an example.

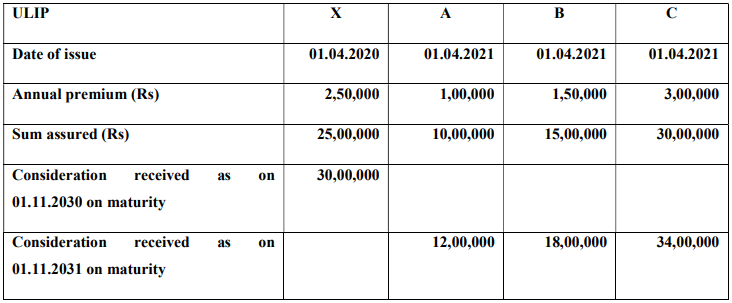

Suppose, an investor had bought an ULIP plan on January 2020 and he buys 3 other plans on March 1, 2021. The details are given in the below table:

Here, investors can claim two exemptions, first being policy X as it was bought before February 2021.

The second exemption can be sought for a combination of policy A and B as their aggregate premium is not more than Rs. 2.5 lakh.

So, at the end the investor will have to pay taxes only on the proceeds received from policy C.

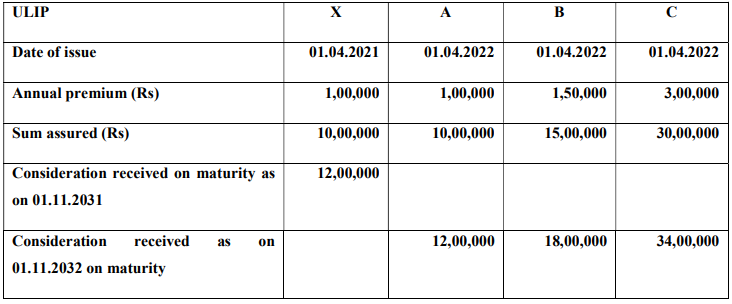

Here's another example for further clarity:

In this example, since all the policies were bought after February 1, 2021, the investor will have to combine two or more policies in such a way that the exemption benefit is highest.

In this case, investors can choose to claim exemption on either X+B or A+B as the aggregate yearly premium of both the combinations is Rs. 2.5 lakh, which is the upper threshold of claiming exemptions.