Is credit quality is a major concern while investing in debt mutual Funds?

The past few years have seen a challenging macroeconomic environment where growth has been slowing while inflation is higher than RBI expectations. Interest rates, tracking inflation, have remained elevated and bank lending rates have remained high despite rate cuts by the Reserve Bank of India. The combination has meant that corporate profitability has taken a hit in recent quarters as well as years.

1. Corporate financial performance has deteriorated and various measures of profitability and interest cover are even worse than in 2008-09 during the crisis period. This deterioration is even before the current rate hikes and liquidity tightening measures introduced by RBI.

The deterioration of corporate financial performance has profound implications for debt fund investors. Ever greater numbers of companies are finding it difficult to keep making payments on debt. This has led to an increase in the number of debt restructurings and non-performing loans at banks. Lower rated corporates are more likely to default than AAA rated corporates and investors must pay attention to credit quality of debt portfolios. Lower rated debt may offer higher yields, but investors should remember that those high yields may themselves be contributing to the financial difficulties of the borrowers.

2. This has led to a spate of rating downgrades and rating agencies have warned about the ability of several companies to meet interest and debt repayment obligations.

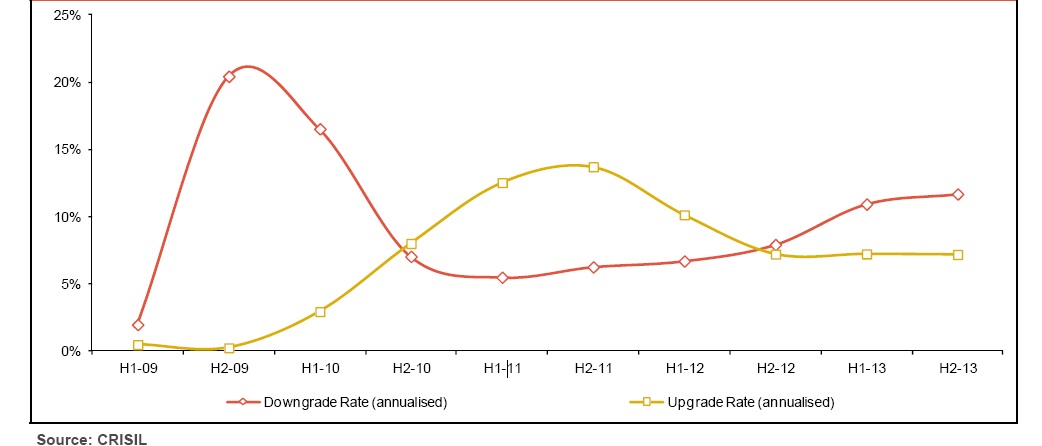

Downgrade rate peaks in H2 2012-13; downgrades will continue to outnumber upgrades over the medium term.

As per the 2012-credit-ratings-trends-round-up published by CRISIL, downgraded ratings on 616 firms in H2 2012-13, as against 484 downgrades in H1 2012-13, indicating that credit quality constraints remained even in H2 2012-13 – defaults accounted for around one third of downgrades in this period. Also, more than 70 percent of downgrades are from ‘BB’ and below rating categories. However, the annual downgrade rate is expected to have peaked at 11.7 percent in H2 2012-13, with the worst seemingly left behind. The downgrades were driven largely by a slowdown in demand and tight liquidity on account of stretched working capital cycles. Demand pressures are expected to ease in the next fiscal, which most likely will restrict a further increase in downgrades. On the other hand, the unwinding of working capital cycles will not happen quickly, which will restrict any sharp increase in upgrades.

Upgrade rate remained at the same level of 7.2 percent in both the halves of 2012-13. The upgrades in H2 2012-13 were on account of improved business performance due to stabilization of past capital expenditure and discipline in debt servicing. More than 80 percent of the upgrades were from rating categories ‘ CRISIL BB’ and below. Furthermore, the upgrades rate for ‘CRISIL D’ was about 13 percent.

The chart appended below showcases the trends in rating actions.

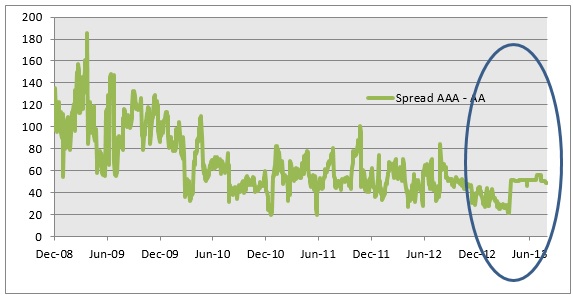

3. The spread between yields on AAA and lower rated debt is low relative to the spreads seen in 2008-09. In sum, we believe that as investors we are not being adequately rewarded for investing in lower rated papers at this time.

It is also pertinent to note that in a credit cycle the extra yield on poorly rated companies (the spread) over AAA increases as credit quality deteriorates. Rising spread could take away some or part of the gain to be had from higher yield as lower rated debt underperforms higher rated debt. Similarly in an economic recovery as financial performance improves and risk is reduced, spreads compress and lower rated debt outperforms.

Currently spreads are low indicating that the extra yield on lower rated debt probably does not justify the poor financial health of these companies. The chart below shows the spread of AA rated papers relative to AAA rated debt for 5-year maturity. (Source: Bloomberg).

Sources: Bloomberg

Mutual fund investments are subject to market risks, read all scheme related documents carefully.