Ratios which Investors should consider while choosing Mutual Fund Schemes

by Mirae Asset Knowledge Academy

Investing by considering only historical returns in a mutual fund scheme is risky. Investors need to evaluate the risk involved in mutual fund schemes before investing. There are no of ratios which mutual fund investors should consider before making their investments. In this article we will cover Treynor Ratio

Definition:

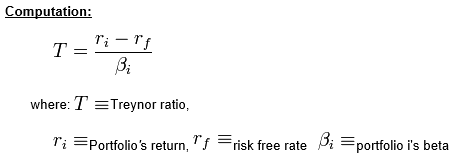

Treynor ratio is also known as reward-to-volatility ratio, Treynor ratio is the excess return generated by a fund over and above the risk free return (government bond yield). It is similar to Sharpe ratio though one difference is that it uses beta as a measure of a measure of volatility. The ratio is named after Jack L. Treynor

The higher the Treynor ratio, the better the performance of the portfolio under analysis.

For example: Your investor gets 7 per cent return on her investment in a scheme with a beta of 1.0. We assume risk free rate is 5 per cent.

Treynor Ratio is 7-5/1.0 = 2 in this case.

Significance

A fund with a higher Treynor ratio implies that the fund has a better risk adjusted return than that of another fund with a lower Treynor ratio.

- Treynor measure and Jenson model use systematic risk based on the premise that the unsystematic risk is diversifiable. These models are suitable for large investors like institutional investors with high risk taking capacities as they do not face paucity of funds and can invest in a number of options to dilute some risks.

- Sharpe measure considers the entire risks associated with fund are suitable for small investors, as the ordinary investor lacks the necessary skill and resources to diversify. Moreover, the selection of the fund on the basis of superior stock selection ability of the fund manager will also help in safeguarding the money invested to a great extent.

Investors are often advised to pick investments with high Treynor ratios.

Sharpe ratios, along with Treynor ratios and Jensen's alphas, are often used to rank the performance of portfolio or mutual fund managers.

Weaknesses

Like the Sharpe ratio, the Treynor ratio does not quantify the value added, if any, of active portfolio management. It is a ranking criterion only. A lot of investors evaluate funds based on Jensen Alpha, which is the value added by the fund manager.

We will be explaining Jensen’s Alpha ratio in our next week article.

Mutual fund investments are subject to market risks, read all scheme related documents carefully.