In our last article we covered Equity Linked Saving Scheme (ELSS) and it features, in the current article we will discuss Public Provident Fund (PPF) in comparison to ELSS.

What is PPF?

The public provident fund (PPF) is a scheme of the Central Government, framed under the PPF Act of 1968. It is one such long-term investment option that would suit investors of all types. Scoring high on safety, by virtue of it being government backed, this wonderful option comes with tax benefits, loan options and a low maintenance cost.

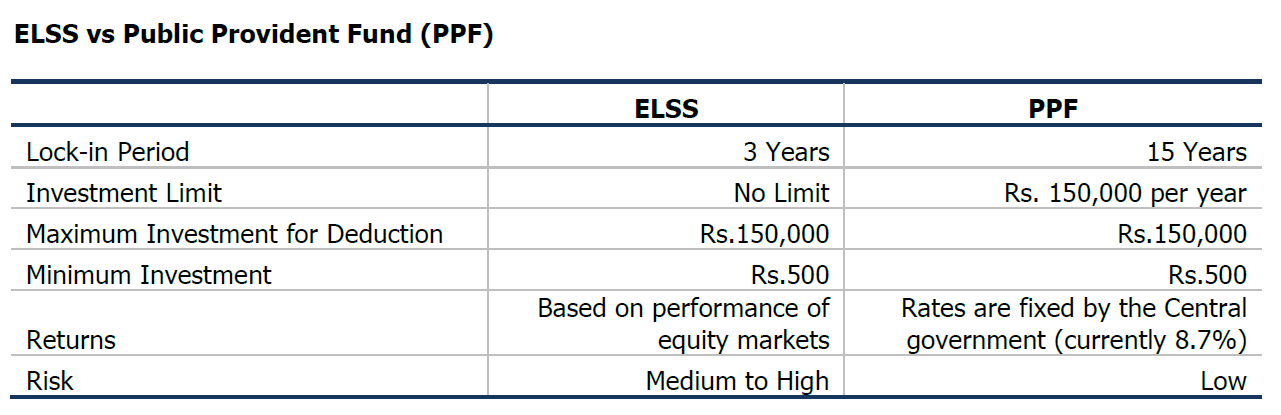

It features in tax saving investment options under Sec 80C of the Income Tax Act, wherein tax payers can save tax on investment of up to Rs.150,000 every year. The lock in period of the scheme is as long as fifteen years and can be extended in block of five years after maturity. Partial withdrawals can be made on the commencement of the seventh year. The scheme mostly invests in both government and corporate bonds and securities and is a debt scheme.

Since the return in PPF is guaranteed and is backed by the government, there is low risk associated with it. However any investor who parks too much money in fixed-income assets can face other types of risk such as inflation risk. A high rate of inflation would erode the value of your savings. Then there is the issue of liquidity too - should the investor need the money for some emergency it would be difficult since the PPF has a lock-in period of 15 years.

PPF Returns:

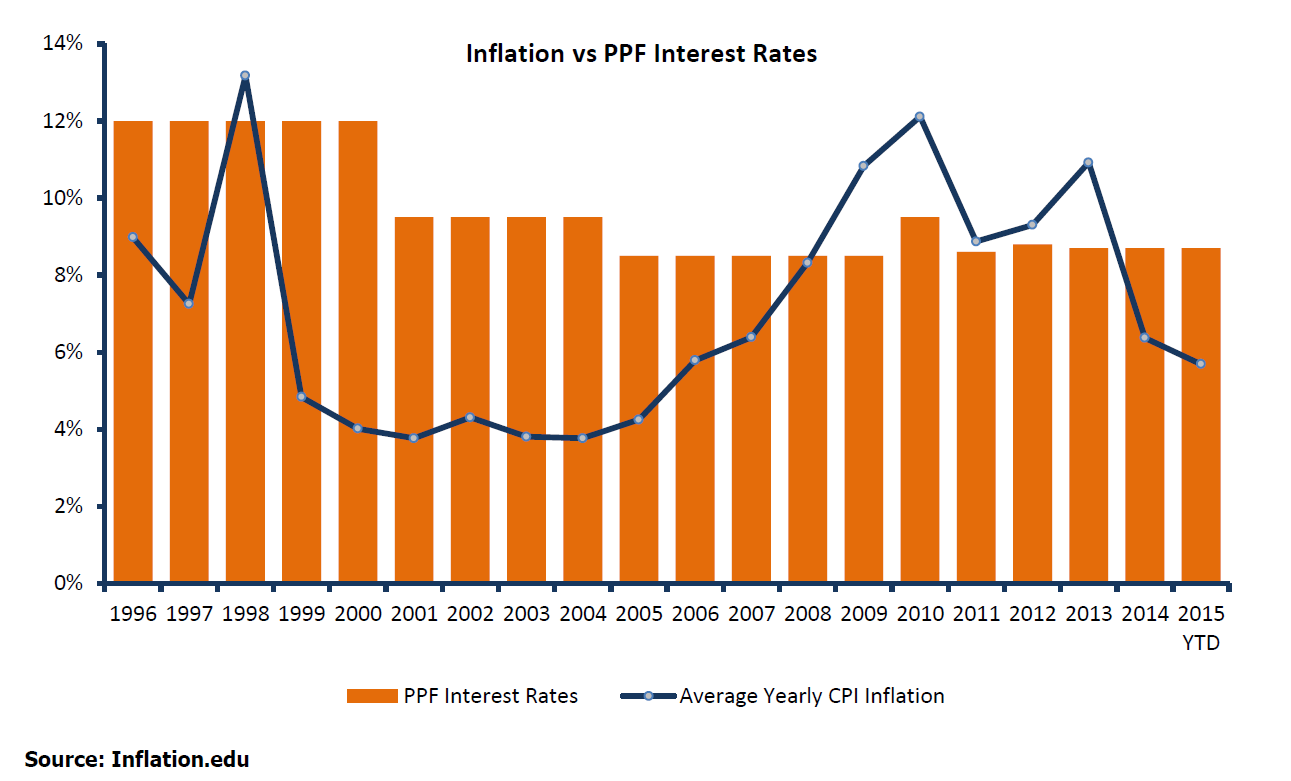

The return in PPF has declined over the years. From 12% at the turn of the century, it dropped down to 11%, then 9.5%, 9% and finally 8% where is languished for many years. Between FY12 and FY15 the rate hovered between 8.6% and 8.7%.

If you take the average inflation by year, the CPI from 2008 to 2013 has fluctuated between 8.32% and 12.11%. All in all, the PPF has not done an excellent job in consistently beating inflation over the last few years.

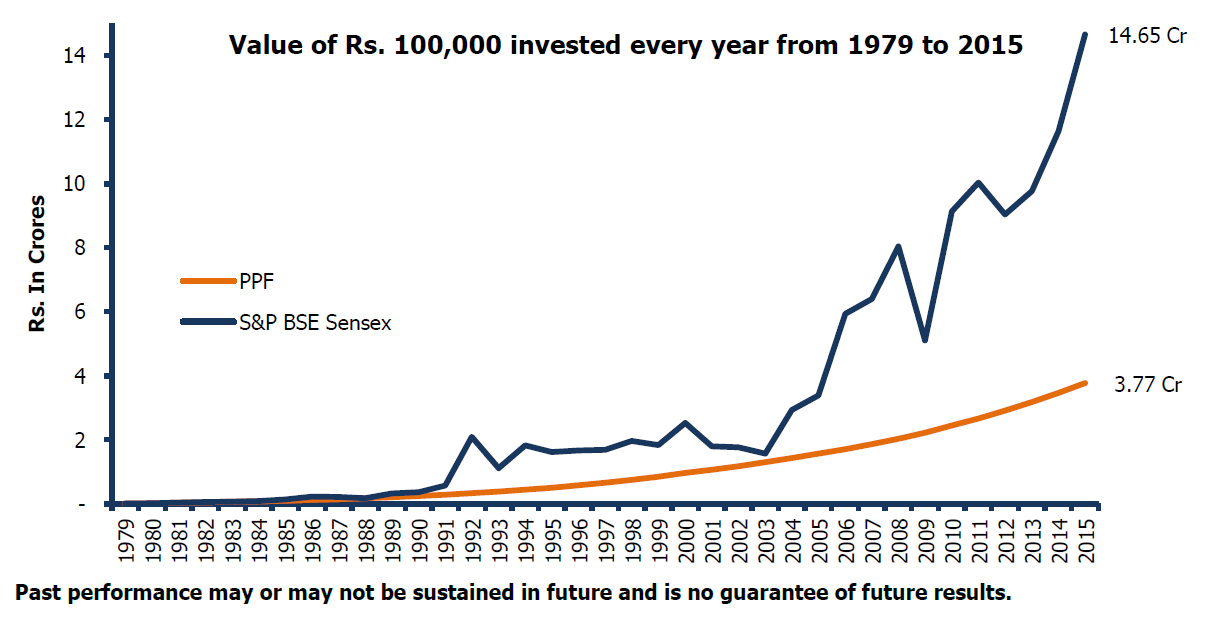

Historically, equities have delivered reasonably better result than PPF:

Source: Bloomberg & www.ppfaccount.in, 1st April 2015. The above graph shows valuation of investment in PPF & S&P BSE Sensex from 1979 to 2015. Rs 100,000 have been invested every year on 1st April (or next business day) in PPF and S&P BSE Sensex.

Should you invest in PPF or ELSS?

Both PPF and ELSS have their merits and demerits. Your investment choice should be informed by your investment objectives and your risk tolerance level. Your risk tolerance level is based on several factors like Age and financial situation

Investors with high risk tolerance should invest in ELSS, while investors with low risk tolerance should invest in PPF. Over a long time frame wealth creation potential is much higher with ELSS, as we saw in the charts above.

- Young investors should opt for ELSS, since they usually have high risk tolerance and a sufficiently long time horizon to ride out the volatilities associated with equity investments.

- As you approach retirement, your risk tolerance goes down and PPF is a better investment option in such a situation.

- Investors with moderate risk tolerance level can invest in both PPF and ELSS in accordance with their optimal asset allocation strategy.

- Salaried individuals are mandatorily required to contribute a portion of their salary to employee provident fund (EPF). The EPF interest rate is similar (slightly lower) to the PPF interest rate and the maturity amount is tax free. The EPF contribution of the employee as well as PPF and ELSS investments goes towards the section 80C tax savings. Accordingly the investors can opt for ELSS, unless they are near retirement. Investment in ELSS through systematic investment plans (SIPs) over a long time horizon will help you both in tax planning and retirement planning.

- Investment horizon is another important consideration, in deciding between PPF and ELSS. The tenure of PPF is 15 years with very limited liquidity during the term of the investment. If you have an investment horizon of 5 to 10 years for any specific financial objective, then reliance on PPF is not advisable. ELSS may be a good investment choice for a 5 to 10 year time horizon, provided it is suitable for your risk profile.

Disclaimers:

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Features of Equity Linked Saving Scheme (ELSS) are subject to either the provisions of the Income Tax Act, 1961 or ELSS guidelines; and are subject to amendments, from time to time.

The information contained in this document is compiled from third party sources and is included for general information purposes only. Any reliance on the accuracy or use of such information shall be done only after consultation to the financial/tax consultant to understand the specific tax implications.