Listen to this article

In the last one year, distributors have led new equity SIP additions in top 30 cities (T-30) but have slightly lagged behind direct investment platforms in rest of the locations (B-30), shows a CAMS report which captures data from mutual funds serviced by the RTA.

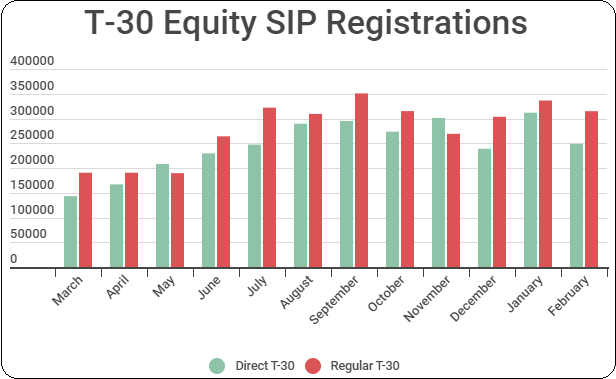

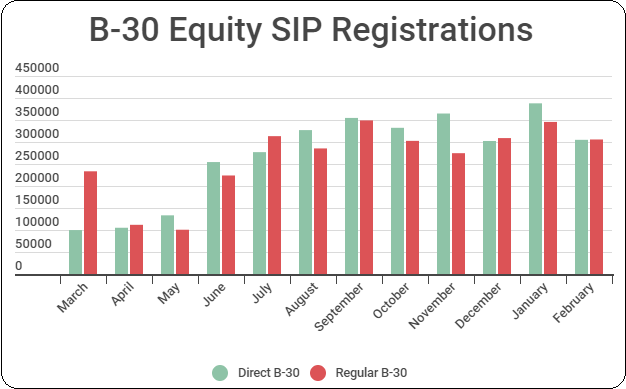

Between March 2021 and February 2022, regular plans accounted for 53% of the total equity SIP registrations in T-30 locations. In the case of B-30 locations, the ratio stood at 49%, the report showed.

Overall, distributors including individual MFDs, banks and NDs accounted for 51% of the total equity SIP registrations during the period.

The study is in line with the results of our recent analysis of AMFI data. The study showed that distributors accounted for registration of the largest chunk of SIPs during January-December 2021. They accounted for over 52% of new registrations (equity and debt).

The data indicates that distributors have maintained their hold on the industry despite stiff competition from online platforms selling direct plans.

Source: CAMS | Charts capture data only from CAMS serviced mutual funds