With SEBI's Potential Risk Class (PRC) matrix, mutual funds have disclosed the risk level of each of their debt schemes.

The PRC matrix, which aims at enhancing transparency with respect to risks in debt schemes, can be an important tool for MFDs to identify the best suitable scheme for their clients.

While risk-o-meter of the fund is a filter that can be used to assess the risk of the portfolio, it has some limitations when it comes to debt funds like it is based on the latest month-end portfolio of the fund and incorporates the interest rate risk, credit risk and liquidity risk of the portfolio. Risk-o-meter does not capture the maximum risk that a debt fund can take.

This is where PRC matrix comes into picture.

Here are some questions which IDFC Mutual Fund has answered to help you know how to assess the “maximum” risk in debt funds.

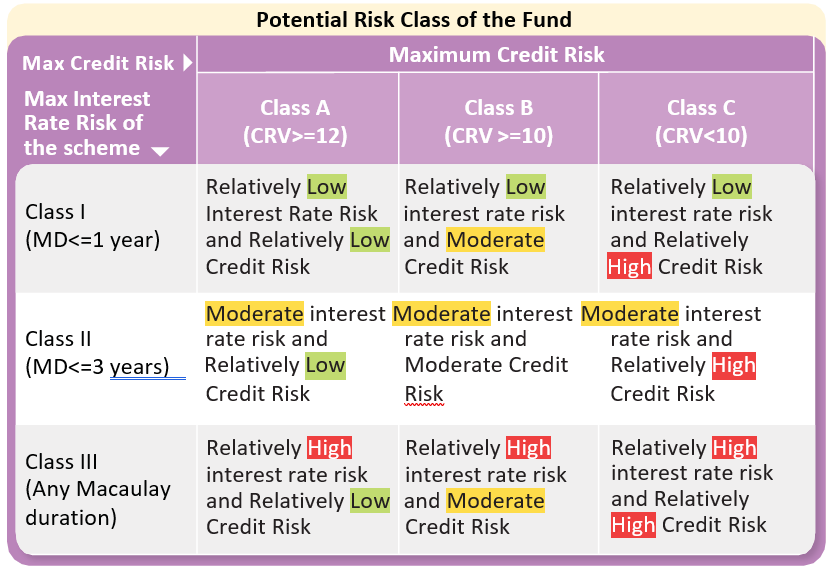

What is PRC matrix?

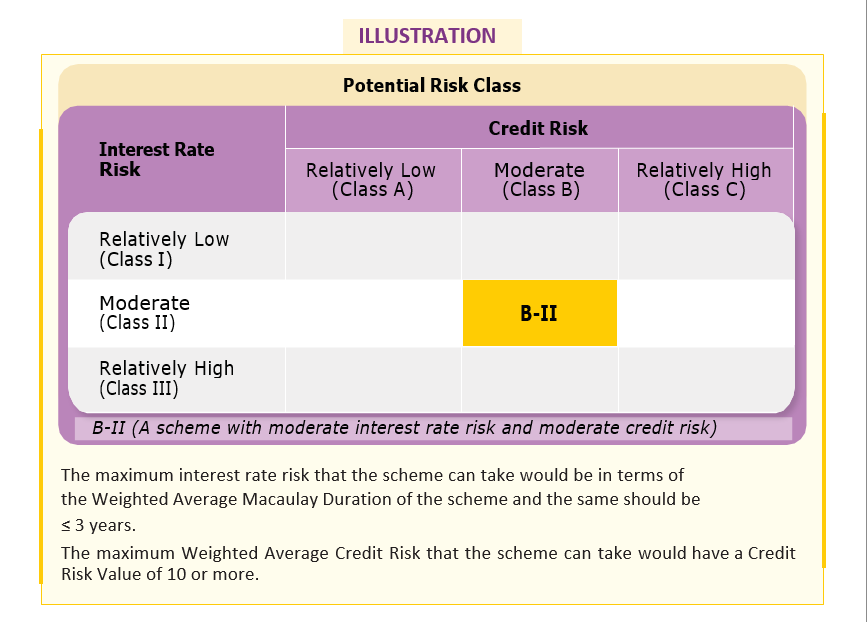

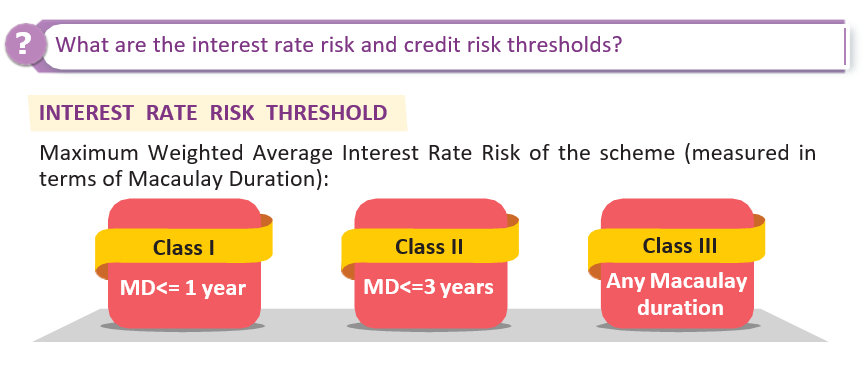

In 2021, SEBI circular made it mandatory for mutual funds to classify all debt schemes in terms of a Potential Risk Class (PRC) matrix. This, in our opinion, is the apt way to measure the maximum level of risk a fund can take. It is a simple yet powerful 3*3 grid, where one axis measures the maximum interest rate risk (measured by Macaulay Duration (MD) of the scheme) while the other axis captures the maximum credit risk that the scheme intends to take at any point in time.

What does each grid in the PRC Matrix stand for?

In Class I, the maximum residual maturity of each instrument held by the scheme should be three years; Class II, the maximum residual maturity of each instrument held by the scheme should be seven years; Class III can invest in instruments of any maturity. (These are not applicable for Central/State government securities).

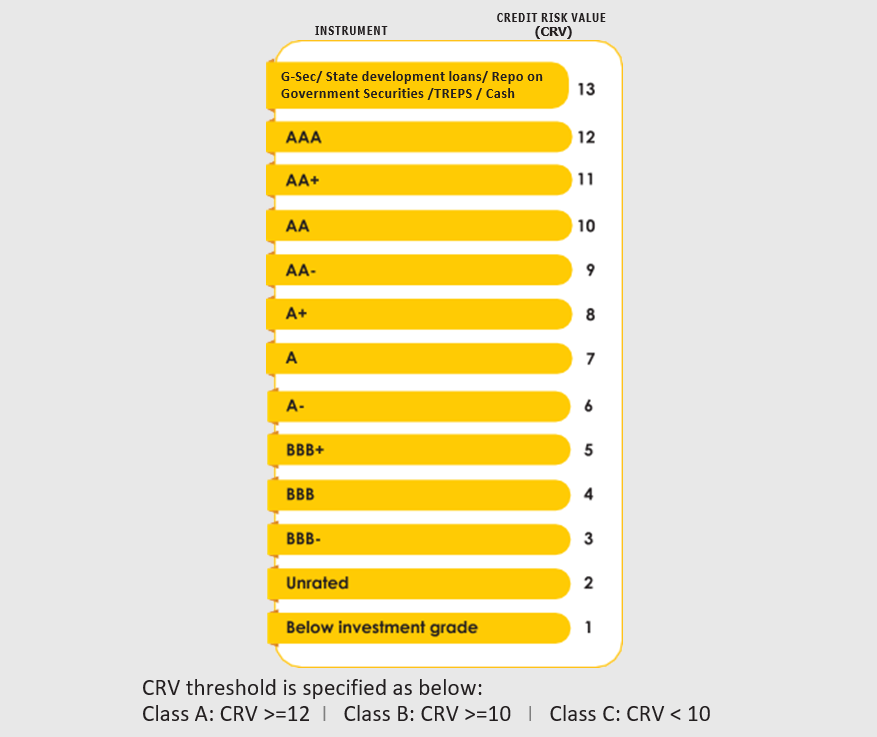

CREDIT RISK THRESHOLD

The Credit Risk Value (CRV) of the scheme shall be the weighted average of the credit risk value of each instrument in the portfolio of the scheme. CRV scores should be based on the lowest long-term rating of an instrument.