A Wealth-X and Arton Capital report estimates that more than 14,000 UHNWIs are likely to pass on US$3.9tn to the next generation in the next decade, equal to the value of the 10 largest companies in the world.

An UHNWI is defined as one with a net worth of US$30m or more.

The average UHNWI is nearly 60 years old. Given that over 60% of these individuals are wealthy due to a self-made business, many will be considering the transfer of significant wealth for the first time.

The Wealth-X and Arton Capital report gives in-depth insights on UHNWI’s philanthropic trends. The report shows that on average, ultra-high net worth individuals (UHNWIs) donate close to US$30m in their lifetimes.

Where do UHNWIs donate?

Education remains by far the most popular philanthropic cause for UHNWIs, followed by health. Environmental issues are an increasingly important cause, especially among the younger generation. UHNW women do direct a higher proportion of giving to the arts, culture and humanities, yet the top five causes (education, higher education, health, arts, culture & humanity and social benefit) remain the same for both genders.

More than half (57%) of the world’s major donors are based in the Americas, which reflects the longstanding tradition of public giving in the US. Across Europe, the Middle East and Africa (EMEA), where welfare states are more prevalent, major donors are thinner on the ground – amounting to less than a fifth of the global total. Asia-Pacific is home to around a quarter of the world’s UHNWIs (51,515), and 4,500 of these are estimated to be major donors.

How do UHNWIs donate?

A raft of innovative financial vehicles has been developed in recent years to make giving simpler and more tax efficient, from donor advice funds (DAFs) to social impact bonds and programme-related investments (PRIs). Many of these new products are hybrids – combining aspects of traditional philanthropy with tools more familiar to investment professionals. Here are some of the popular investment vehicles for philanthropy:

- Programme-related Investments

PRIs are investments made by foundations to support charitable activities that involve the potential return of capital within an established timeframe. They often include financing methods associated with banks or other private investors, such as loans, loan guarantees, linked deposits, and even equity investments in charitable organisations or in commercial ventures for philanthropic purposes. PRIs tend to be set up by donors aiming to supplement existing grant programmes, where the charity or enterprise has the potential to generate income to repay a loan at low rates of interest. Affordable housing and community development are among the most common beneficiaries of PRIs.

- Donor-Advised Funds (DAFs)

DAFs are philanthropic vehicles that allow donors to make a charitable contribution, receive an immediate tax benefit and then recommend grants from the fund over time. They could be described as a form of charitable savings account: a donor contributes to the fund whenever they wish and then recommends grants to their favourite philanthropic cause. Developed in the US, they have become very popular in recent years, with myriad specialist providers offering legal and compliance services.

- Social Impact Bonds

Social impact bonds are financial vehicles that enable investors to pay for interventions that aim to address social problems. If the social outcome improves, the municipal authority or whoever commissioned the bond repays the investors for their initial investment plus a return for the financial risks they took. If the social outcomes are not achieved, the investors stand to lose their investment. As such, in terms of investment risk, social impact bonds are closer to equity investments.

The first social impact bond was launched by Social Finance UK in 2010 and targeted reducing reoffending (commit another offence). They have steadily gained ground, notably among public sectors that are committed to innovation, data and evidence. By mid-2016, 60 social impact bonds, or Pay for Success projects as they are known in the US, were launched in 15 countries. They target issues such as criminal justice, homelessness, child welfare, and youth development.

- Pooling Resources

Another innovation is collaborative philanthropy – the sharing of data, best practices, needs and skills to maximise the impact of giving. Traditionally, UHNWIs have tended to build autonomous, independent entities that are designed to address specific issues. Collaborative organisations such as the Network of European Foundations are breaking the mould and, in some cases, linking with governments to scale up philanthropic activities and avoid duplication.

Going ahead

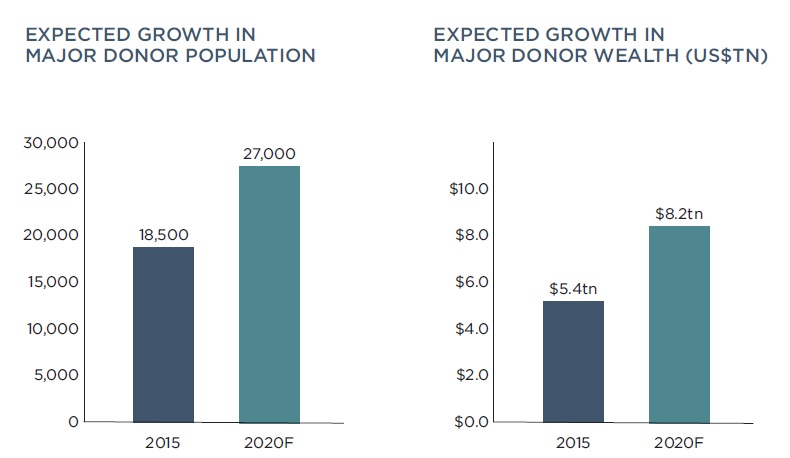

If the group of ‘major donors’ (who have donated at least US$1m in their lifetime) continues to expand at the same rate as the overall UHNW population, in five years’ time they will have grown by around 50% to 27,000 individuals. As a group, they would be worth more than US$8tn in 2020, a rise of nearly US$3tn – greater than the GDP of the UK, or nearly double the GDP of the Gulf Cooperation Council (GCC). Based on the current average lifetime giving of US$30m, this means an additional US$260bn will potentially be in play for philanthropic causes in the coming years.

Edited excerpts from Wealth-X Arton Capital 2016 Changing Philanthropy report.